1 vs 3 Credit Cards: Which Strategy Builds Your Score Faster?

Jun, 25 2026

Jun, 25 2026

Credit Utilization Calculator: 1 vs. 3 Cards

See how spreading your spending across multiple credit cards lowers your utilization rate compared to using a single card.

Imagine you have a choice between one master key that opens every door in your house, or three specialized keys-one for the front door, one for the garage, and one for the safe. Which setup gives you more control? For many people, managing credit feels like holding just that single master key. They rely on one card for everything, from groceries to gas, assuming simplicity is king. But when it comes to building a robust credit score, simplicity can sometimes work against you.

The question of whether to hold one credit card or three isn't about hoarding plastic; it's about strategy. Your credit score is not a random number assigned by banks. It is a calculated prediction of your reliability as a borrower. To get the best score, you need to optimize specific variables that scoring models look at. Having multiple accounts, specifically three well-managed ones, often provides a mathematical advantage over having just one. However, this advantage only exists if you know exactly how to manage them.

The Math Behind Credit Utilization

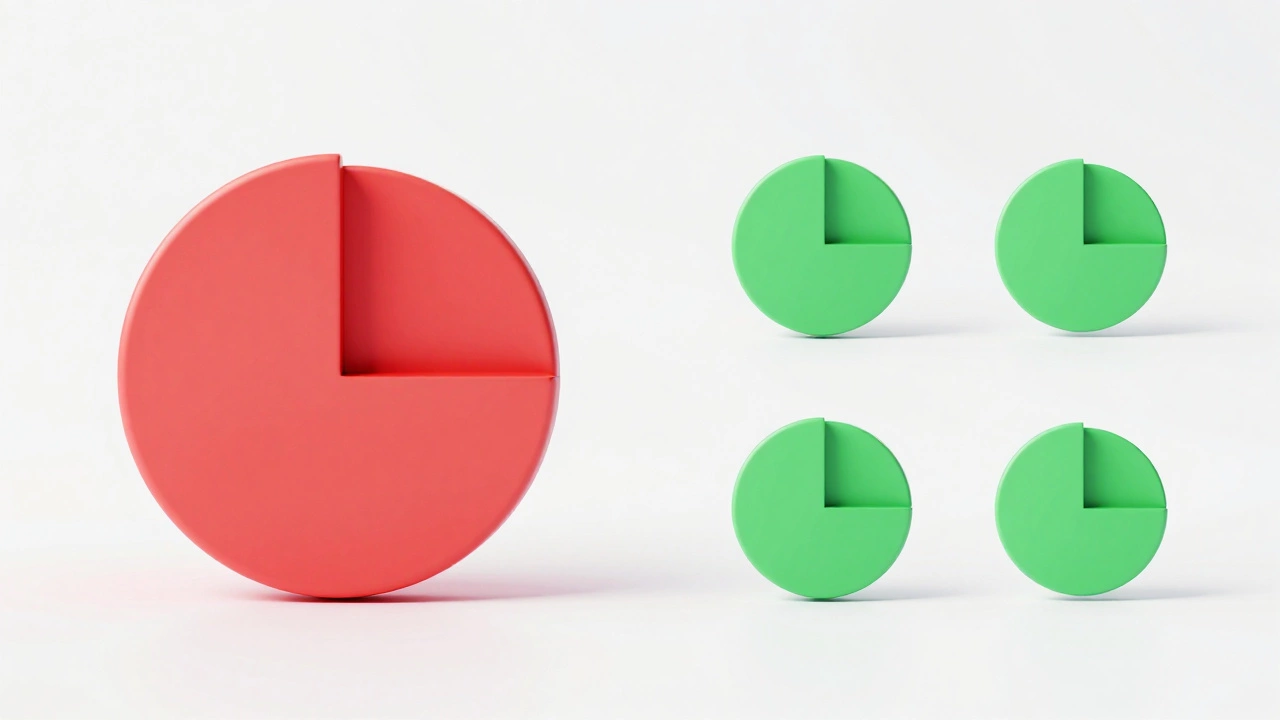

If there is one rule that dominates credit scoring, it is utilization. This metric measures how much of your available credit you are currently using. Most experts agree that keeping this number below 30% is crucial, but aiming for under 10% is even better for top-tier scores. Let’s look at why three cards beat one here.

Suppose you have a single credit card with a $5,000 limit. You buy a new laptop for $1,500. Your utilization jumps to 30%. If you then go on vacation and spend another $1,000, your utilization hits 50%. Suddenly, your credit report tells lenders you are half-maxed out. That looks risky. Now, imagine you have three cards, each with that same $5,000 limit. Your total available credit is $15,000. You still spend that same $2,500 on the laptop and vacation. But now, your utilization is only 16.6%. The debt amount hasn’t changed, but the risk profile has dropped significantly because your capacity to handle debt is higher.

| Scenario | Total Limit | Balance Spent | Utilization Rate |

|---|---|---|---|

| One Card | $5,000 | $2,500 | 50% |

| Three Cards | $15,000 | $2,500 | 16.6% |

This math works in your favor instantly. By spreading your spending across three cards, you keep your individual account utilizations low and your overall ratio healthy. Just remember, you must pay off the balances in full every month to avoid interest charges. The benefit is in the reporting, not in carrying debt.

Credit Mix and Diversification

Scoring models also like variety. This factor is known as "credit mix." Lenders want to see that you can handle different types of credit responsibly. While installment loans (like car loans or mortgages) count toward this, revolving credit (credit cards) is the other half of the equation. Within revolving credit, diversity helps too.

Having three cards allows you to tailor each one to a specific purpose without cluttering your life. You might use one card for travel rewards, another for cash back on groceries, and a third for everyday purchases where you want extended warranty protection. This diversification shows lenders you can manage distinct relationships with different issuers. If all three cards are from the same bank, the benefit is slightly reduced, but the credit limit boost remains. Ideally, you want two or three cards from different major networks-Visa, Mastercard, and perhaps American Express-to show broad compatibility.

Think of it like an investment portfolio. Putting all your money into one stock is risky. Spreading it across a few stable companies reduces volatility. Similarly, relying on one credit line means if that issuer lowers your limit or closes your account due to inactivity, your entire credit foundation shakes. With three cards, you have redundancy. If one goes down, you still have two others maintaining your credit age and limits.

The Power of Average Age of Accounts

Here is where the "one card" strategy actually shines, and why adding cards requires caution. One of the most important factors in your credit score is the average age of your accounts. Older accounts are generally viewed more favorably because they provide a longer track record of behavior. When you open a new credit card, it starts at zero months old. This drags down your average age, causing a temporary dip in your score.

If you have had one credit card for ten years, opening two new cards will lower that average age immediately. However, this impact is usually short-lived. Over time, those new cards age alongside your original one. The long-term benefits of higher credit limits and diversified usage typically outweigh the initial hit to your account age. The key is patience. Don't apply for three cards all on the same day unless you are prepared for a small, temporary score drop. Space out applications by six months or more if possible. This way, each card begins its aging process separately, minimizing the shock to your credit file.

Furthermore, never close your oldest card. That original account is the anchor of your credit history. Even if you rarely use it, keep it open and active. Make a small purchase on it once every few months and pay it off. This keeps the account current and preserves that valuable length of history.

Risks of Managing Multiple Cards

More cards mean more responsibility. The biggest risk with holding three credit cards is not the scoring model; it is human error. It is easy to forget a statement date, miss a payment, or lose track of which card was used for which expense. A single missed payment can slash your credit score by hundreds of points and stay on your report for seven years. No amount of strategic utilization can recover from negligence.

To manage three cards effectively, you need a system. Set up automatic payments for the minimum amount due on all three cards. This ensures you never miss a deadline. Then, manually review your statements monthly to catch errors and ensure you are staying within your budget. Use a personal finance app or a simple spreadsheet to track spending across all accounts. If you find yourself overwhelmed by juggling three login portals, consider sticking to two cards until you build better habits. Quality of management always trumps quantity of accounts.

Hard Inquiries and Approval Odds

Every time you apply for a credit card, the issuer performs a "hard inquiry" on your credit report. This is a check that signals you are seeking new credit. Too many hard inquiries in a short period can signal financial distress to lenders, suggesting you are desperate for funds. Most scoring models allow for a cluster of inquiries within a short window (like 14-45 days) to be counted as one for rate shopping purposes, but this does not always apply to credit card applications depending on the specific scoring version used.

Applying for three cards simultaneously will result in three hard inquiries. This might make it harder to get approved for a fourth card or a mortgage soon after. If your credit is already thin or fair, applying for three cards at once could lead to rejections, which adds negative marks to your file. A smarter approach is to start with one solid card, build a positive history for six to twelve months, and then add the second and third cards gradually. This demonstrates responsible growth rather than sudden expansion.

When One Card Is Actually Better

Is there ever a case where one card is superior? Yes. If you struggle with impulse spending, having multiple cards can increase your temptation to overspend. Seeing three high limits might subconsciously encourage you to spend more than you can afford. In this scenario, the psychological safety of a single card with a strict limit is invaluable. It forces discipline.

Additionally, if you have a very short credit history, say less than two years, adding multiple accounts might complicate your profile unnecessarily. Focus on mastering one relationship first. Prove you can pay on time and keep balances low. Once you have established that baseline, expanding to two or three cards becomes a powerful tool for optimization. For students or young adults just entering the workforce, a single secured credit card or student card is often the best starting point.

Building Your Ideal Three-Card Portfolio

If you decide to move forward with three cards, structure them intentionally. Do not just pick three random offers. Think about coverage. A balanced portfolio might look like this:

- The High-Limit Anchor: A card with a high credit limit that you use sparingly. Its primary job is to inflate your total available credit, lowering your utilization rate. Keep the balance near zero.

- The Everyday Driver: A card with good rewards for daily expenses like groceries and gas. Use this for recurring bills to earn points while paying them off immediately.

- The Specialty Card: A card tailored to a specific large expense, such as travel or dining. This helps you maximize returns on discretionary spending without affecting your main driver.

This setup ensures you are not putting all your eggs in one basket. If the airline changes its loyalty program, your travel card loses value, but your grocery and general cards remain unaffected. It also spreads the risk of fraud. If one card is compromised, you can freeze it while continuing to use the others without disrupting your entire financial life.

Does having more credit cards hurt my credit score?

Not necessarily. While opening new cards causes a temporary dip due to hard inquiries and lowered average account age, having more cards can significantly boost your score long-term by increasing your total credit limit and lowering your credit utilization ratio. The net effect is usually positive if you manage the accounts responsibly.

Should I use all three cards equally?

No, you do not need to use them equally. In fact, it is often better to concentrate spending on one or two cards to maximize rewards, while keeping the third card mostly unused to maintain a high credit limit with low utilization. Just ensure you make at least one small transaction on each card annually to keep them active.

What is the ideal number of credit cards for a perfect score?

There is no magic number, but data suggests that individuals with FICO scores of 800+ typically have around 7 credit cards. However, you do not need seven to achieve a great score. Three to five well-managed cards are usually sufficient to optimize utilization and credit mix without creating unmanageable complexity.

Can I improve my score faster with one card or three?

You can likely improve your score faster with three cards because of the immediate boost to your available credit limit. This lowers your utilization ratio quickly, which is a major weighting factor in credit scoring models. With one card, hitting low utilization requires either a very high limit or very low spending.

Do annual fees matter when choosing between 1 and 3 cards?

Yes. If you choose three cards, try to minimize annual fees unless the rewards clearly outweigh the cost. Carrying three cards with $95 fees each costs $285 a year. Ensure the cash back, points, or travel credits you earn exceed this amount. Otherwise, stick to no-fee cards to keep your net financial position strong.