Are Student Loans Still on Hold in 2024? The Truth About Payments and Relief

May, 31 2026

May, 31 2026

Student Loan Payment & SAVE Plan Estimator

Loan Details

Your Estimated Results

Estimated Standard Monthly Payment (10-year term @ ~5%):

Estimated SAVE Plan Payment:

Analysis:

Enter your details to see if you qualify for low or zero payments.

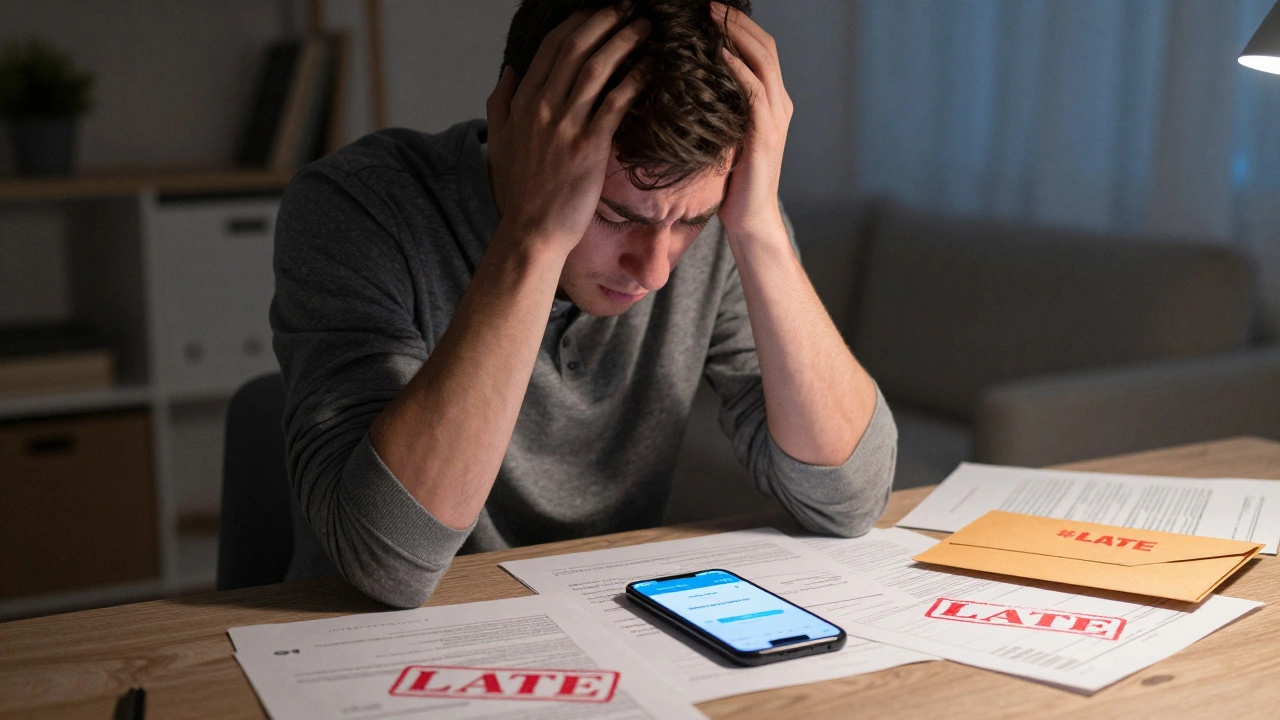

If you have been waiting for a clear answer on whether student loan payments are still paused, the short answer is no. The era of widespread automatic forbearance ended months ago. For most borrowers, the hold on student loans is officially over. If you missed the recent notifications from your servicer, you might be facing late fees or credit score impacts right now. It is easy to feel overwhelmed by the shifting rules, but understanding exactly where things stand can help you avoid costly mistakes.

The confusion stems from a long period of uncertainty. From March 2020 through December 2023, interest rates were frozen at 0% and monthly payments were suspended due to the pandemic. This was known as the administrative pause. When that pause lifted, many expected immediate chaos. Instead, the Department of Education extended the deadline. Now, we are well past those dates, and the landscape has changed significantly. You need to know if your specific loans require action today.

The End of the Automatic Pause

The federal government’s decision to end the broad payment suspension marked a major shift. The original pause expired in January 2022, but it was extended multiple times. The final extension pushed the resumption of payments to November 2023. However, even then, not everyone had to pay immediately. Borrowers who were already enrolled in an Income-Driven Repayment (IDR) plan often saw their payments drop to $0 based on their updated income information. For these individuals, the "pause" felt like it continued because their bills were negligible.

For borrowers on standard repayment plans or those who had not updated their financial data, the reality was different. Servicers sent out letters warning that payments would resume. Many people ignored them, hoping for another extension. There were no further extensions. By early 2024, millions of Americans were back on the hook for their monthly obligations. If you are asking if loans are still on hold in 2024, the answer is a definitive no for the vast majority of federal borrowers.

Did the student loan pause extend into 2024?

No, the federal student loan payment pause did not extend into 2024. The final extension ended with the resumption of payments in November 2023. Any borrower expecting a new automatic pause in 2024 was mistaken, though some may have qualified for zero-dollar payments under new IDR plans.

Why Some People Feel Like They Are Still Paused

You might hear friends or colleagues saying they do not have to pay anything. This creates confusion. Why does it seem like some people are still on hold while others are paying hundreds of dollars a month? The reason lies in the new repayment options introduced alongside the end of the pause. The Department of Education launched the Saving on a Valuable Education (SAVE) plan. This is an income-driven repayment option that calculates your monthly payment based on your discretionary income.

Under the SAVE plan, if your annual income is below a certain threshold-specifically, 225% of the Federal Poverty Level for a single borrower-your required monthly payment is $0. This is not a pause; it is a calculated payment amount. You are still actively repaying your loan, but the system determines your contribution is zero for now. Interest may still accrue on unsubsidized loans, but the government pays any remaining unpaid interest on subsidized loans. This distinction is crucial. You are not in forbearance; you are in a repayment plan that happens to cost you nothing this month.

This nuance explains why social media feeds are full of mixed messages. Someone with a low income and a high debt balance might genuinely owe $0 per month. Another person with a higher income or private loans owes their full scheduled amount. Both are technically "repaying," but only one feels the burden. Understanding this difference helps you figure out where you fit in the spectrum.

The SAVE Plan: Your Best Tool for Low Payments

If you are struggling with your current payment amount, the SAVE Plan is likely your best option. Unlike previous IDR plans, SAVE offers more generous calculations. It considers half of your discretionary income rather than 10% or 15%. Furthermore, it protects borrowers with smaller balances. If you have a balance of $12,000 or less, your loan could be paid off in ten years without making a single dollar of principal payments, thanks to how interest is handled.

To qualify, you must submit an application to your loan servicer. This involves providing proof of your income, usually via tax transcripts. The process is straightforward but requires attention to detail. Do not assume you are automatically enrolled. Even if you were on a previous IDR plan, you might need to re-enroll or switch to SAVE to get the benefits. Many borrowers stayed on older plans like Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE) simply because they forgot to update their status. These older plans often result in higher monthly payments compared to SAVE.

Consider Sarah, a teacher in Ohio with $45,000 in student debt and an annual salary of $48,000. Under her old REPAYE plan, she paid $150 a month. After switching to SAVE, her payment dropped to $0. She is not in default, nor is she in forbearance. She is actively managing her debt through a plan designed for her income level. This scenario is common among public sector workers, recent graduates, and those in lower-wage industries.

Private Loans: No Pause, No Forgiveness

All the discussion above applies to federal student loans. If you have private student loans, the rules are completely different. Private lenders, such as banks or credit unions, never participated in the federal payment pause. Their contracts remained active throughout the pandemic. If you have private loans, you have been expected to make payments since March 2020. Missing those payments likely resulted in late fees, increased interest rates, and damage to your credit score.

Private loans also do not offer income-driven repayment plans like SAVE. You cannot apply for forgiveness based on income or career service. Your options are limited to negotiating directly with the lender. Some lenders offered temporary hardship programs during the economic downturn, but these were voluntary and varied widely. Today, if you are behind on private loans, you need to contact your servicer immediately. Ask about deferment options, which might allow you to pause payments for six to twelve months, but interest will continue to accrue. Unlike federal loans, there is no safety net here.

| Feature | Federal Loans | Private Loans |

|---|---|---|

| Payment Pause Ended | November 2023 | Never existed |

| Income-Driven Plans | Yes (e.g., SAVE) | No |

| Interest Accrual During $0 Payment | Limited (Govt pays excess on subsidized) | Full accrual |

| Forgiveness Options | Yes (PSLF, IDR) | No |

| Credit Reporting | Paused reporting until late 2023 | Continuous reporting |

Credit Score Impact and Reporting

One of the biggest worries for borrowers returning to repayment is how it affects their credit scores. During the pause, federal loan servicers stopped reporting positive payment history to credit bureaus. This meant that making payments (if you chose to) did not boost your score, but missing them did not hurt it either. That changed when payments resumed. Since late 2023, federal loans have been reported again. On-time payments build your credit history. Late payments damage it.

If you fell behind before the pause ended, do not panic. The Department of Education implemented a policy to prevent immediate delinquency reporting for borrowers who were current before the pause. However, if you have missed payments since November 2023, those will show up on your credit report. Check your credit reports from Equifax, Experian, and TransUnion regularly. Dispute any errors immediately. If you see a late payment listed that should have been covered by a valid deferment or IDR plan, file a dispute with the bureau and provide documentation from your servicer.

Building good habits now is essential. Set up automatic payments if possible. Even small amounts count toward keeping your account in good standing. If you cannot afford the full amount, contact your servicer to adjust your plan before you miss a payment. Proactive management prevents the spiral of late fees and credit damage.

What To Do If You Cannot Afford Your Payments

If you are staring at a bill you cannot pay, you have options. First, check if you qualify for the SAVE plan. If your income is low enough, your payment might drop to zero. Second, consider general deferment or forbearance. Deferment is available for specific situations, such as returning to school or economic hardship. Forbearance is a broader option that allows you to pause payments for up to twelve months, but interest continues to capitalize. Use forbearance sparingly, as it increases your total debt burden.

Another strategy is refinancing. If you have excellent credit and a stable income, you might refinance your federal loans into a private loan with a lower interest rate. Be cautious here. Refinancing federal loans means losing access to federal protections like IDR plans and forgiveness programs. Only do this if you are confident you can repay the loan without needing those safety nets. For most borrowers with significant debt or unstable incomes, staying within the federal system is safer.

Finally, seek counseling. Non-profit credit counseling agencies can help you create a budget and negotiate with creditors. Avoid debt settlement companies that promise to wipe out your debt for a fee. These services often charge high upfront costs and can worsen your financial situation. Stick to reputable resources like the Consumer Financial Protection Bureau (CFPB) or accredited non-profits.

Looking Ahead: Stability Over Surprise

The volatility of the last few years has made planning difficult. However, the current framework provides more stability than the constant extensions of the past. The rules for the SAVE plan and other IDR options are established. While political debates continue regarding potential future changes, the existing laws govern your loans today. Relying on hope for a new pause is a risky strategy. Assume you will need to manage your debt according to current regulations.

Taking control of your student loans starts with accurate information. Know your loan types, your servicer, and your repayment options. Log in to National Student Loan Data System (NSLDS) to view all your federal loans. Contact your servicer to discuss your budget. Whether you are paying $0 under SAVE or $500 on a standard plan, being informed reduces stress and improves outcomes. The pause is over, but your path to financial freedom is just beginning.

Will there be another student loan pause in 2026?

There is no official announcement of a new federal student loan pause for 2026. Current policies require borrowers to make payments unless they qualify for a $0 payment under an income-driven plan like SAVE. Borrowers should plan based on the assumption that payments are active.

Does the SAVE plan forgive my entire loan?

The SAVE plan does not forgive your loan immediately. It caps your monthly payments based on income. Remaining balances may be forgiven after 20 years (or 10 years for undergraduate-only debt), but this forgiveness may be taxable depending on current tax laws.

How do I check if my loans are in good standing?

Log in to your loan servicer's website or visit the National Student Loan Data System (NSLDS) to view your loan status. Ensure your contact information is up to date so you receive important notices about payment resumption or plan changes.

Can I consolidate my loans to lower my payment?

Federal Direct Consolidation Loans can simplify payments by combining multiple loans into one. However, consolidation itself does not lower interest rates. To lower payments, you must enroll in an IDR plan like SAVE after consolidating. Note that consolidation resets the clock on Public Service Loan Forgiveness (PSLF) progress for some loans.

What happens if I miss a payment in 2024?

Missing a payment results in a late fee and potential negative impact on your credit score. After 90 days of non-payment, your loan enters default. Default leads to wage garnishment, tax refund offsets, and loss of eligibility for further aid. Contact your servicer immediately if you miss a payment to discuss rehabilitation or consolidation options.