What Does It Mean to Remortgage Your House in 2026?

Understand what remortgaging means in Canada, including the difference between switching lenders versus refinancing, and how to manage penalties.

Read MoreEver heard the word “remortgage” and thought it sounded complicated? It’s basically swapping your current mortgage for a new one – often with a different lender – to get a better deal. Think of it as refinancing your car loan, but for your house.

If you’re paying a high interest rate or want to free up some cash, a remortgage can be a handy tool. The key is knowing when it actually helps and what costs you might face.

First, look at your current rate. If you locked in a 5% deal five years ago and the market is now offering 3.5%, you could slash your monthly payments. Lower rates also mean you’ll pay less interest over the life of the loan.

Another common reason is borrowing more. Say you’ve built up equity and need extra cash for a renovation or to consolidate debt. A remortgage can let you tap into that equity, often at a lower rate than a personal loan.

But it’s not always a win. If you’re close to the end of your mortgage term, the savings might be modest. Also, early‑repayment charges on your existing deal can eat into any benefit.

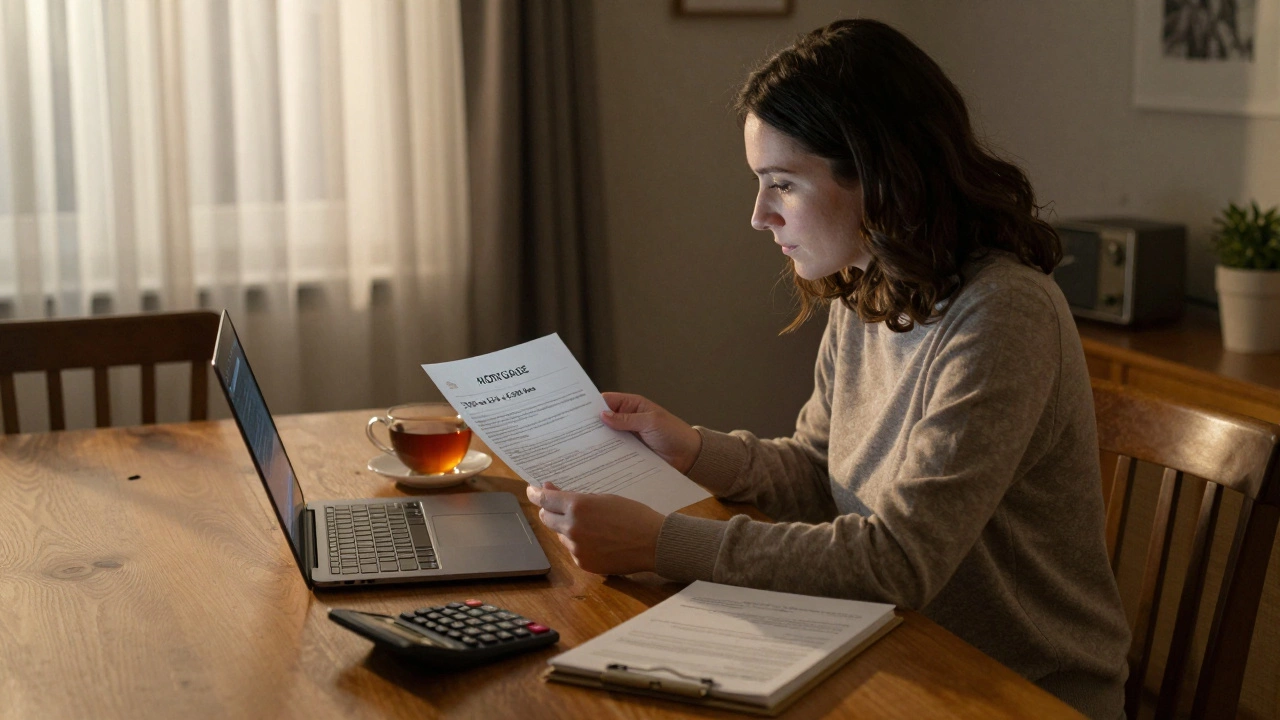

Remortgaging isn’t free. Typical fees include arrangement fees (often a few hundred pounds), valuation costs, and possibly a broker’s fee if you use one. Some lenders waive fees for high‑value loans, so it pays to shop around.

Don’t forget the “hidden” costs: legal fees for the transfer, stamp duty on any extra cash you borrow, and potential early‑repayment penalties from your current lender. Adding these up before you decide will give you a realistic picture of the net saving.

If you’re trying to borrow less instead of more, the process is similar but you might face lower fees because the loan size is smaller. This can help you reduce debt faster and free up cash flow.

Many homeowners wonder whether remortgaging is easier than applying for a brand‑new mortgage. In practice, the paperwork is a bit lighter – the lender already knows the property – but you still need to prove income, creditworthiness and meet affordability tests.

Overall, the decision boils down to three questions: Is the new rate lower enough to offset fees? Do you need extra cash, or can you afford to pay less each month? And can you meet the lender’s criteria without too much hassle?

Take a look at your mortgage statement, jot down the current rate, and compare it with today’s market offers. Use an online calculator to estimate savings after fees. If the numbers look good, talk to a few lenders or a broker to get quotes. Remember, the cheapest deal isn’t always the best – consider flexibility, early‑payoff options, and any special features you might need.

Bottom line: Remortgaging can lower payments, free up equity, or both, but only if you do the math and watch out for fees. A little research now can save you a lot of money later.

Understand what remortgaging means in Canada, including the difference between switching lenders versus refinancing, and how to manage penalties.

Read More

Is it better to remortgage with your existing lender? Often, staying put saves fees and hassle-but only if you ask for the right deal. Learn when to stay and when to switch.

Read More

To remortgage in Canada, you typically need at least 20% equity in your home. Learn how to calculate your equity, what lenders require, and what to do if you don't meet the threshold.

Read More

There's no legal limit to how many times you can remortgage your house in Canada - but each time costs money and risks your equity. Learn when it makes sense, when to avoid it, and how to protect your home’s value.

Read More

Learn the exact signs that it’s time to remortgage, how to calculate savings, key factors to check, and a step‑by‑step guide for Toronto homeowners.

Read More

Not sure what remortgaging means? This article breaks down remortgaging in plain English, covering why people do it, how it works, and who it makes sense for. Get clear tips, spot common slip-ups, and understand how remortgaging could impact your finances short and long term. Straightforward info, no fluff—just practical answers about whether this move is right for you.

Read More

Thinking about squeezing more money out of your home when you remortgage? This article breaks down how lenders decide what you can borrow, the key factors that shape your options, and common pitfalls to watch out for before you sign anything new. Find out how much extra cash you could unlock and what you’ll need to get approval. Get tips for boosting your borrowing power without getting in over your head.

Read More

Thinking of remortgaging? There might be some fees involved, and knowing these costs beforehand can save you from unexpected surprises. This article explores the types of remortgage fees, what they cover, and tips on how to minimize them. Along the way, we’ll also share some handy advice to help you navigate the remortgaging process smoothly.

Read More

Wondering if a 4.75% interest rate is a good deal for your mortgage? This article breaks down the factors to consider, including historical averages, market trends, and personal financial situations. Discover when a 4.75% rate can work in your favor and tips to potentially secure even better deals. Dive into how this rate could affect your monthly payments and overall loan cost. Understand the significance of shopping around for the best rates and what to watch out for in mortgage agreements.

Read More

Navigating the world of mortgages can be as complex as a maze, with options like remortgaging providing a potential shortcut. This article explores whether remortgaging is indeed easier than securing a new mortgage. We dive into interesting facts, compare processes, and offer practical tips on making the best choice. Discover what to consider, potential benefits, and how to make your next financial move smoother.

Read More

Remortgaging involves switching an existing mortgage to a new one, typically with a different lender, to secure better terms or rates. Homeowners often consider this option to reduce monthly payments, free up equity, or pay off a mortgage sooner. However, it's crucial to weigh the costs, benefits, and potential risks carefully. By examining key factors and expert advice, individuals can make informed decisions about whether remortgaging suits their financial goals.

Read More

If you find yourself needing to borrow more money but don't want to go through the hassle or cost of remortgaging, there are several alternative routes to consider. From homeowner loans to credit unions and secured or unsecured personal loans, each option comes with its own set of benefits and caveats. Understanding these options can help you decide the best approach for your financial situation. This article delves into these potential solutions, offering insights and tips to make informed decisions.

Read More