What Are 30-Year Mortgage Rates Right Now? (July 2026 Guide)

Jul, 5 2026

Jul, 5 2026

Mortgage Payment & Cost Calculator

Loan Details

Based on July 2026 estimates:

6.6% - 6.8%

6.8% - 7.0%

7.0% - 7.3%

7.3% - 7.8%

Estimated Results

Monthly Principal & Interest

Effective Rate Used

Buying a house is expensive. The monthly payment you see on a listing isn't the whole story. It’s just the principal and interest. But what drives that number up or down? The interest rate. Specifically, for most buyers, it’s the 30-year fixed mortgage rate. If you are looking at homes today in July 2026, you need to know where those rates actually sit. They aren’t static. They shift based on bond markets, inflation data, and central bank decisions. Getting this wrong can cost you tens of thousands of dollars over the life of the loan.

The short answer? As of early July 2026, average 30-year fixed mortgage rates are hovering around 6.8% to 7.1%. This is higher than the historic lows we saw a few years ago, but slightly lower than the peaks of 2024. However, averages are misleading. Your actual rate depends on your credit score, down payment, and whether you pay points to buy the rate down.

Why Do Mortgage Rates Change Daily?

You might notice that rates change every single day. Sometimes they jump by a tenth of a percent overnight. Why does this happen? Mortgage lenders don’t set rates out of thin air. They follow the market. Specifically, they look at the 10-year U.S. Treasury yield. Think of the Treasury yield as the baseline risk-free return investors get for lending money to the government. Lenders want to make more than that to cover their risks. So, when Treasury yields go up, mortgage rates usually follow.

What exactly determines my specific mortgage rate?

Your specific rate is determined by the base market rate plus adjustments for your personal financial profile. Key factors include your credit score, debt-to-income ratio, loan amount, property type, and how much cash you put down.

In 2026, the Federal Reserve has kept its benchmark interest rate steady after a long period of hikes. While the Fed doesn’t directly control mortgage rates, its actions influence the broader economy. When the Fed signals that inflation is under control, bond markets calm down, and mortgage rates often drop slightly. Conversely, if economic data shows strong job growth or rising prices, investors worry about future inflation, sell bonds, and rates climb.

Current Rate Landscape: What You Can Expect in July 2026

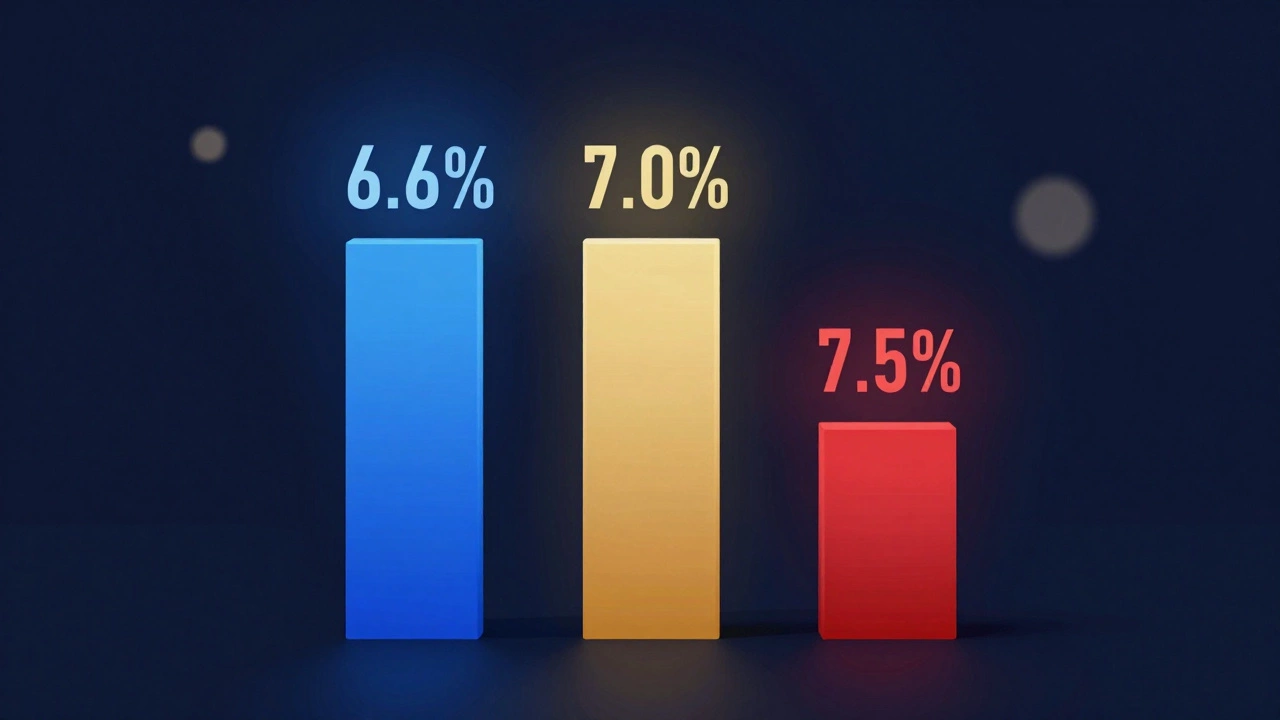

Let’s break down what "current" means. National averages from major aggregators like Freddie Mac and Bankrate show the 30-year fixed rate sitting near 6.95%. But here is the catch: these are national averages. They include people with perfect credit scores and large down payments. They also include people with lower scores who pay more.

If you have a credit score above 760, a 20% down payment, and a conventional loan, you might see offers closer to 6.6% or 6.7%. If your credit score is below 680, or if you are using an FHA loan with minimal down payment, expect rates closer to 7.2% or higher. Jumbo loans-those exceeding the conforming loan limits-often carry slightly different pricing because they aren’t backed by Fannie Mae or Freddie Mac. In some markets, jumbo rates are competitive; in others, they are significantly higher.

| Credit Score Range | Estimated Interest Rate | Monthly Payment per $100k Borrowed |

|---|---|---|

| 760+ | 6.6% - 6.8% | $~$635 |

| 720-759 | 6.8% - 7.0% | $~$655 |

| 680-719 | 7.0% - 7.3% | $~$675 |

| Below 680 | 7.3% - 7.8%+ | $~$700+ |

Note that these numbers do not include taxes, insurance, or PMI (Private Mortgage Insurance). If you put less than 20% down, you will likely pay PMI, which adds another $50-$150 a month depending on your loan size and state.

Fixed vs. Adjustable: Is 30 Years Still the Best Choice?

With rates in the high 6s, many buyers are asking if they should switch to an adjustable-rate mortgage (ARM). A 5/1 ARM, for example, locks in a fixed rate for five years, then adjusts annually. Today, 5/1 ARMs are offering rates roughly 0.5% to 0.75% lower than 30-year fixed loans. That could mean starting at 6.2% instead of 6.9%.

This sounds attractive. But there is a risk. After five years, the rate resets based on market conditions. If rates stay low, you save money. If rates climb again, your payment could spike. Most financial advisors suggest ARMs only if you plan to sell or refinance before the adjustment period begins. If you intend to stay in the home for 10+ years, the predictability of a 30-year fixed rate is usually worth the slightly higher initial cost.

How Much Does a 0.25% Difference Really Cost?

We talk about rates in terms of percentages, but what does that mean for your wallet? Let’s say you are borrowing $400,000. At 6.9%, your monthly principal and interest payment is about $2,600. At 7.15%, it jumps to $2,670. That seems small-just $70 a month. But over 30 years, that difference adds up to nearly $25,000 in extra interest.

This is why shopping around matters. Don’t just take the first quote you get. Get Loan Estimates from at least three different lenders. Banks, credit unions, and online-only lenders all price loans differently. Some have lower overhead and pass savings to you. Others charge higher fees to offset a lower advertised rate. Always compare the Annual Percentage Rate (APR), which includes fees, not just the nominal interest rate.

Strategies to Lower Your Rate in 2026

You can’t control the market, but you can control your application. Here are practical steps to secure the best possible rate right now:

- Boost your credit score: Even a 20-point increase can drop your rate by 0.1% to 0.25%. Pay down credit card balances to keep utilization below 30%. Check your reports for errors and dispute them.

- Make a larger down payment: Putting 20% down eliminates PMI and signals lower risk to lenders. If you can afford 25% or 30%, you may qualify for even better pricing.

- Buy discount points: You can pay upfront fees (points) to lower your interest rate. One point equals 1% of the loan amount. On a $400,000 loan, one point costs $4,000 but might lower your rate by 0.25%. Calculate the break-even point. If you plan to stay in the home longer than the break-even period, it makes sense.

- Reduce your debt-to-income (DTI) ratio: Lenders prefer a DTI below 43%. Pay off small debts like car notes or personal loans before applying. This strengthens your profile and gives you negotiating power.

- Lock your rate strategically: Rates fluctuate daily. If you see a rate you like, ask your lender about a rate lock. Standard locks last 30-60 days. If closing takes longer, you may need to extend the lock, which sometimes carries a fee. Watch the 10-year Treasury yield closely. If it drops sharply, call your lender immediately.

Refinancing: Should You Move Your Existing Mortgage?

If you already have a mortgage, you might be wondering if refinancing makes sense. In 2026, the answer is mostly no-if your current rate is below 6%. Refinancing involves closing costs, typically 2%-5% of the loan amount. To recoup those costs through monthly savings, you need a significant rate drop. Unless your credit has improved dramatically or you can pay points to buy down the new rate, staying put is usually smarter.

However, if you locked in a rate above 7.5% during the volatility of 2024-2025, refinancing might help. Run the numbers. Use a refinance calculator to determine your break-even point. If you plan to move within two years, refinancing rarely pays off.

Regional Differences Matter

Mortgage rates aren’t uniform across the country. Lenders adjust rates based on local real estate markets. In hot markets where home prices are rising fast, lenders perceive higher risk and may charge slightly more. In slower markets, competition among lenders can drive rates down. Additionally, property taxes and insurance costs vary wildly by state. While these don’t change your interest rate, they affect your total monthly housing expense. A low rate in California might still result in a high payment due to taxes and insurance.

Looking Ahead: Will Rates Drop Further?

No one knows for sure. Economists are divided. Some believe the Federal Reserve will cut rates later in 2026 if inflation continues to cool toward the 2% target. Others warn that sticky services inflation could keep rates elevated. The consensus among most mortgage experts is that rates will remain in the 6.5% to 7.5% range for the foreseeable future. The era of 3% mortgages is likely over for now.

This reality check changes how we approach home buying. We need to focus on affordability rather than chasing the lowest possible rate. Budget conservatively. Assume rates could rise slightly before you close. Build a buffer into your emergency fund. And remember: a house is a place to live, not just an investment vehicle. Emotional satisfaction matters too.

Common Mistakes to Avoid

Many borrowers make costly errors when navigating the current rate environment. Avoid these pitfalls:

- Applying for multiple credit cards before buying: Each hard inquiry can ding your credit score. Space out credit applications.

- Changing jobs mid-process: Lenders verify employment. Switching jobs can delay closing or cause denial if the new income is unstable.

- Ignoring the APR: The interest rate is just one part. The APR includes origination fees, discount points, and other charges. Compare APRs to get the true cost.

- Waiting for the "perfect" rate: Timing the market is nearly impossible. Rates can swing back against you while you wait. Focus on finding a rate that fits your budget comfortably.

Next Steps for Home Buyers

If you are ready to buy, start by getting pre-approved. This isn’t just a formality. It shows sellers you are serious and capable. Shop around with at least three lenders: a big bank, a local credit union, and an online lender. Ask each for a Loan Estimate within three days of your application. Compare them side-by-side. Look at the interest rate, APR, closing costs, and any lender credits.

Once you choose a lender, monitor the 10-year Treasury yield daily. If it drops significantly, ask your lender if they can match the lower rate. Be prepared to act quickly. Good deals move fast, especially in competitive markets.

Are mortgage rates going down in 2026?

Most economists predict modest declines or stability in 2026, with rates likely remaining between 6.5% and 7.5%. Significant drops below 6% are unlikely unless there is a major economic recession.

What is the best time of year to get a mortgage?

Historically, late fall and winter (November-February) see slightly lower demand for mortgages, which can lead to marginally lower rates. However, seasonal trends are weak compared to macroeconomic factors like inflation and Fed policy.

Should I pay points to lower my rate?

Only if you plan to stay in the home long enough to recoup the upfront cost. Calculate the break-even point: divide the cost of points by the monthly savings. If your planned ownership period exceeds the break-even months, paying points makes financial sense.

How does my credit score affect my mortgage rate?

Credit scores are tiered. Scores above 760 typically get the best rates. Scores between 680-759 face slightly higher rates. Below 680, rates increase significantly, and options may be limited to FHA or government-backed loans.

Is it better to buy now or wait for lower rates?

If you find a home you love and can afford the payment at current rates, buying now is reasonable. Waiting for lower rates risks missing out on inventory or facing higher home prices. Remember, you can always refinance later if rates drop significantly.