What Are the Drawbacks of a Debt Consolidation Loan?

Mar, 16 2026

Mar, 16 2026

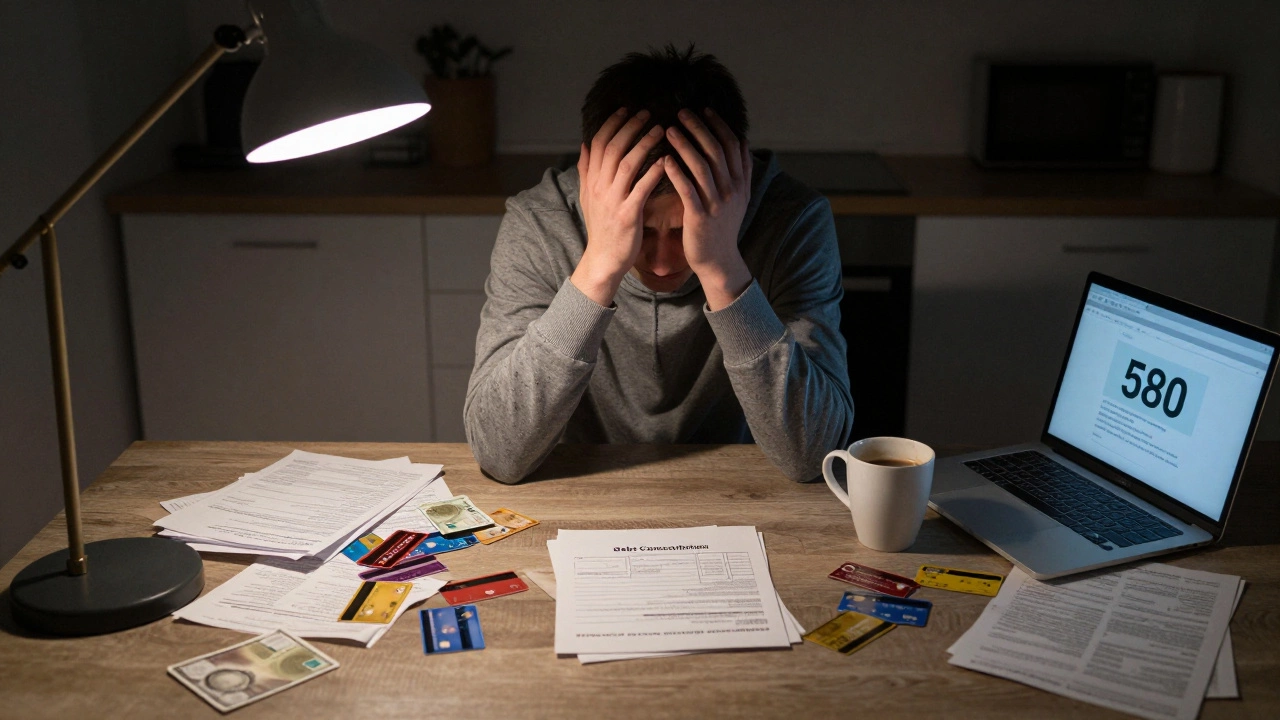

Debt consolidation loans sound like a lifesaver. You pile up all your credit card balances, medical bills, or personal loans into one payment with a lower interest rate. It’s simple, clean, and makes sense on paper. But here’s the truth: debt consolidation loan isn’t a magic fix. For many people, it makes things worse before they get better.

You’re Still in Debt - Just Rearranged

The biggest mistake people make is thinking consolidation means they’re out of debt. It doesn’t. You’re just swapping one debt for another. If you had $15,000 in credit card debt at 22% interest and took out a consolidation loan at 8%, you’re now paying less each month - but you still owe $15,000. That’s not progress. That’s repackaging.Worse, once that credit card balance hits zero, many people turn around and start charging again. Without changing spending habits, you end up with the original debt plus a new loan. That’s $30,000 in debt instead of $15,000. It happens more often than you think. A 2024 study from the Canadian Credit Union Association found that 43% of people who consolidated debt with a personal loan had new credit card balances within six months.

Extended Repayment = More Interest Paid Over Time

Lower monthly payments feel great. But they often come with a hidden cost: longer repayment terms. Let’s say you had $12,000 in credit card debt. You were paying $400 a month and clearing it in 3 years. Now you take a 5-year consolidation loan at 7% with a $240 monthly payment. You’re saving $160 a month - nice. But over the full term, you’ll pay $2,180 in interest. On the original plan, you paid just $1,320. You saved money upfront, but paid $860 more in the long run.This isn’t about being cheap. It’s about being realistic. If you can’t afford the original payments, maybe you need a different solution - like a debt management plan through a nonprofit credit counselor. Stretching out the debt doesn’t solve the problem. It just hides it.

Secured Loans Put Your Home or Car at Risk

Some lenders push you toward a secured consolidation loan. That means you pledge something valuable - usually your home or car - as collateral. If you miss payments, they can take it. That’s not a small risk. In Toronto, home equity loans have surged since 2023, and defaults on secured debt rose 18% last year.People think, “I’ve got equity - I’m safe.” But equity isn’t cash. It’s paper. If your income drops, your car breaks down, or you get sick, that “safe” loan becomes a foreclosure notice. A 2025 report from the Financial Consumer Agency of Canada showed that 29% of people who took secured consolidation loans ended up in arrears within two years. That’s nearly one in three.

Not Everyone Qualifies - And If You Don’t, You’re Worse Off

You can’t just walk into a bank and get a low-rate consolidation loan. Lenders check your credit score, income, and debt-to-income ratio. If you’re already struggling with debt, your credit score is probably already damaged. Many people apply for a consolidation loan, get denied, and then apply for multiple loans in quick succession. Each application drops your score another 5-10 points.By the time they find a lender willing to approve them, they’re stuck with a high-interest loan - often worse than what they started with. I’ve seen clients come in with $10,000 in credit card debt at 24%, get denied for consolidation, then take a 28% payday loan to cover the gap. That’s not progress. That’s a spiral.

Fees Can Eat Your Savings

Some consolidation loans come with origination fees, prepayment penalties, or administrative charges. These aren’t always obvious. A lender might advertise a 6.9% rate - but charge a 5% origination fee. On a $10,000 loan, that’s $500 upfront. You’re not borrowing $10,000. You’re borrowing $9,500. And if you pay it off early? Some lenders charge you for it.Compare that to a nonprofit credit counseling program. They often restructure your debt with no fees at all. No credit check. No collateral. Just a single payment plan negotiated with your creditors. It’s not glamorous. But it works - and it doesn’t cost you anything.

It Doesn’t Fix the Root Problem

Debt isn’t the illness. Overspending, under-earning, or lack of emergency savings are. A consolidation loan treats the symptom - multiple payments - but ignores the cause. You can have the lowest interest rate in Canada, but if you keep spending more than you make, you’ll be back here in a year.Real change requires budgeting, tracking every dollar, and building a safety net. One client I worked with in Scarborough paid off $18,000 in debt with a consolidation loan. Three months later, she maxed out her credit cards again - because she never learned how to live within her means. She didn’t need a loan. She needed a plan.

What Should You Do Instead?

If you’re thinking about a debt consolidation loan, ask yourself:- Have I stopped using credit cards? If not, consolidation won’t help.

- Can I afford the monthly payment without cutting essentials like food, rent, or medicine?

- Am I willing to freeze my credit cards and not open new ones?

- Have I checked with a nonprofit credit counselor first?

If you answered “no” to any of those, skip the loan. Talk to a credit counselor. They can help you set up a debt management plan that stops collection calls, reduces interest rates, and gives you a clear path out - without putting your home or car at risk.

Debt consolidation loans aren’t evil. But they’re not a shortcut. They’re a tool - and like any tool, they can break your fingers if you use them wrong.

Is a debt consolidation loan right for me if I have bad credit?

If you have bad credit, you’ll likely be offered a high interest rate - sometimes higher than your current credit cards. Many lenders require a credit score of at least 650 for the best rates. If your score is below that, you might end up paying more in interest than you would if you kept your existing debts. Before applying, check your credit report for errors and consider working with a nonprofit credit counselor to improve your score first.

Can I consolidate student loans with a personal loan?

Technically, yes - but it’s usually a bad idea. Federal student loans in Canada come with protections like income-based repayment, loan forgiveness programs, and interest relief during hardship. A personal loan wipes all that out. You might get a lower rate, but you lose flexibility. Only consider this if you’ve already paid off your student loans and are now dealing with private debt from them - and even then, proceed with caution.

How long does a debt consolidation loan affect my credit score?

When you apply for a consolidation loan, the hard inquiry drops your score temporarily - usually by 5 to 10 points. If you open a new account, your average credit age decreases, which can also lower your score. But if you make all payments on time, your score will recover within 6 to 12 months. The real damage comes if you max out your old credit cards again - that can tank your score for years.

Are there alternatives to a debt consolidation loan?

Yes. A debt management plan through a nonprofit credit counselor is one of the best. They negotiate lower interest rates with your creditors, combine your payments into one, and stop collection calls. There’s no credit check, no collateral, and no fees. Another option is a balance transfer credit card with a 0% intro rate - but only if you can pay it off before the promotional period ends. And if you’re overwhelmed, bankruptcy or a consumer proposal might be better than taking on more debt.

What happens if I can’t make the payments on my consolidation loan?

If it’s an unsecured loan, your credit score will drop, and collectors will start calling. If it’s secured - meaning you used your home or car as collateral - the lender can repossess it. Late payments also trigger fees and higher interest rates. The worst part? You’re now behind on two debts: the original ones you tried to consolidate, and the new loan. That’s a trap many people don’t escape from.