What Credit Score Do You Need for Debt Consolidation? (2026 Guide)

Jun, 22 2026

Jun, 22 2026

Debt Consolidation & Credit Score Analyzer

Your Financial Profile

Debt-to-Income Ratio (DTI)

Analysis Results

Enter your financial details and click "Analyze Eligibility" to see your options.

You’re staring at a stack of bills, and the interest rates are eating your monthly payments alive. It feels like you’re running on a treadmill that’s set to sprint speed. You’ve heard about debt consolidation, and it sounds like the lifeline you need-one single payment instead of ten, maybe even a lower interest rate. But then comes the nagging question: "Will they actually approve me?" The answer depends almost entirely on one number: your credit score.

In 2026, lenders in Canada and elsewhere have become more sophisticated with their risk models. They don’t just look at your FICO or Equifax score; they look at your debt-to-income ratio, your recent payment history, and how much credit you’re currently using. If you think there’s a magic number that guarantees approval, I’m here to burst that bubble. There isn’t one. However, there are clear thresholds that determine which doors open and which ones slam shut in your face.

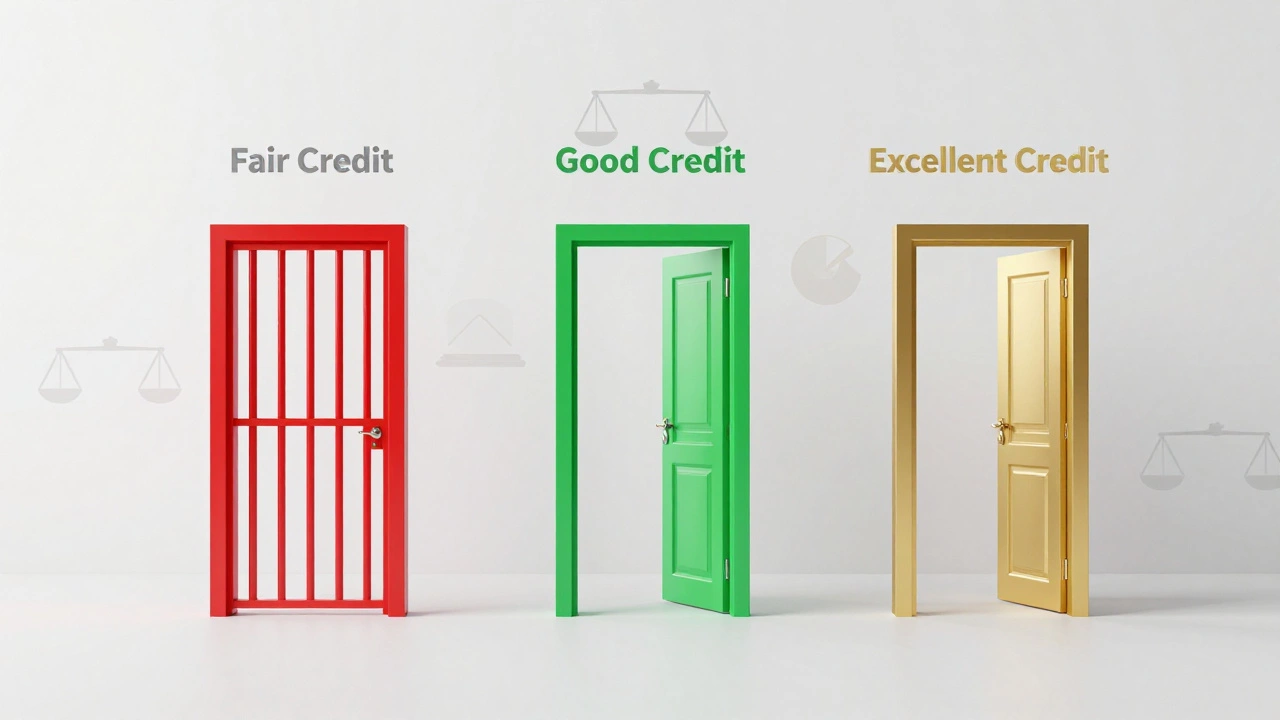

The Reality of Credit Score Thresholds

Let’s get straight to the numbers because that’s what you came for. Lenders generally bucket applicants into three categories when it comes to unsecured debt consolidation loans. These aren’t hard laws, but they are the industry standard for underwriting decisions.

- Fair Credit (580-669): This is the danger zone. You might find a lender, but the interest rate could be higher than what you’re paying now. Many online lenders operate here, but watch out for origination fees that can eat up any savings.

- Good Credit (670-739): This is the sweet spot for most traditional banks and credit unions. You’ll likely qualify for rates between 8% and 14%, depending on market conditions. This is where real savings happen.

- Excellent Credit (740+): You have options. You can shop around for the lowest APRs, often dipping below 8%. You also qualify for premium balance transfer cards with longer introductory periods.

If your score is below 580, traditional unsecured debt consolidation loans are mostly off the table. Don’t panic yet-there are other paths, but they require a different strategy, which we’ll cover later.

| Credit Score Range | Best Option | Estimated Interest Rate (APR) | Approval Likelihood |

|---|---|---|---|

| 740+ | Premium Balance Transfer Card / Low-Loan Bank Loan | 0% intro (15-21 months) or 6-9% | Very High |

| 670-739 | Traditional Personal Loan / Credit Union Loan | 9-14% | High |

| 580-669 | Online Lender Personal Loan / Secured Loan | 15-25% | Moderate |

| Below 580 | Debt Management Plan (DMP) / Family Loan | N/A (Negotiated rates via agency) | Low for new debt |

Why Your Score Isn't the Only Factor

I know, I just gave you the numbers. But if you apply for a loan with a 680 score and get rejected, don’t blame the algorithm immediately. Lenders use a holistic approach. Think of your credit score as the headline, but your financial profile is the full article.

The biggest co-pilot to your credit score is your Debt-to-Income Ratio (DTI). This is the percentage of your gross monthly income that goes toward paying debts. If you make $5,000 a month and pay $2,500 in existing debts, your DTI is 50%. Most lenders want to see a DTI below 36% for the best rates. Some will stretch to 43%, but anything above that makes them nervous. Why? Because they think you’re already stretched too thin to handle another payment, even a consolidated one.

Another factor is your Credit Utilization Ratio. This measures how much of your available credit you’re using. If you have five credit cards with a total limit of $10,000 and you owe $9,000, your utilization is 90%. That screams "risk" to lenders. Interestingly, consolidating debt can help this. If you take out a personal loan to pay off those cards, your credit card balances drop to zero, lowering your utilization and potentially boosting your score over time. It’s a virtuous cycle-if you don’t run up the cards again.

The Two Main Paths: Loans vs. Balance Transfers

When people say "debt consolidation," they usually mean one of two things. Knowing the difference is crucial because they have very different credit score requirements.

Personal Loans: This is the most common method. You borrow a lump sum from a bank, credit union, or online lender and use it to pay off multiple high-interest debts. You then make one fixed monthly payment to the new lender. As noted above, you generally need a score of at least 670 for decent terms. Online lenders are more flexible and may accept scores down to 580, but the cost of borrowing will be significantly higher.

Balance Transfer Credit Cards: This involves moving your existing credit card debt to a new card with a 0% introductory APR period. This is the holy grail of consolidation because you pay no interest for a set time (usually 12 to 21 months). However, these cards are picky. In 2026, most major issuers require a credit score of 700 or higher to approve you for a 0% offer. If your score is below 700, you might still get a card, but it likely won’t have a long 0% intro period, or it might come with a high balance transfer fee (typically 3% to 5%).

What If Your Credit Is Bad?

Let’s say your score is sitting at 550. Maybe you had a medical emergency, a divorce, or just fell behind during economic uncertainty. Does that mean you’re stuck? No. It just means you can’t get a *new* loan to pay off old debt easily. Here are your realistic alternatives:

- Debt Management Plans (DMPs): You work with a non-profit credit counseling agency. They negotiate with your creditors to lower your interest rates and waive late fees. You make one monthly payment to the agency, which distributes it to your creditors. You don’t get a new loan; you keep your existing accounts but under better terms. This works regardless of your credit score, though it does impact your credit report initially.

- Secured Personal Loans: If you have assets-a car, a savings account, or home equity-you can use them as collateral. A secured loan requires less faith in your creditworthiness because the lender has something to take if you default. Home Equity Lines of Credit (HELOCs) are popular here, but remember: you’re putting your house on the line.

- Family or Friends: It’s awkward, but an interest-free loan from a relative can be a lifeline. Just treat it like a bank loan. Sign a simple contract, set a repayment schedule, and pay on time. Missing a payment to your aunt is worse than missing one to Chase.

The Hidden Trap: Behavioral Change

Here’s the part no one wants to talk about. Debt consolidation fixes the *math*, not the *behavior*. If you consolidate your credit card debt into a personal loan, your cards will be paid off. They will have available credit. If you swipe them again while making payments on the loan, you haven’t solved anything. You’ve just added a new layer of debt on top of the old one.

This is why lenders look at your employment history and income stability. They want to know you have the capacity to repay. But you need to ask yourself: Do I have the discipline? Consolidation only works if you close the old accounts or lock the cards in a block of ice. Use the freed-up cash flow to build an emergency fund so you don’t need to borrow next time life throws a curveball.

Steps to Take Before Applying

Don’t just hit "apply" on the first website you see. Every hard inquiry on your credit report drops your score by a few points. Multiple inquiries in a short period signal desperation to lenders. Follow this checklist:

- Check Your Reports: Pull your free reports from Equifax and Experian. Dispute any errors. A mistaken late payment could be dragging your score down artificially.

- Calculate Your DTI: Know exactly how much of your income is tied up in debt. If it’s high, consider cutting expenses before applying to improve your chances.

- Shop Around Within 14 Days: Credit scoring models (FICO and VantageScore) treat multiple inquiries for the same type of loan within a 14-day window as a single inquiry. This allows you to compare rates without penalty.

- Read the Fine Print: Look for prepayment penalties. Some lenders charge you for paying off the loan early. You want a loan that rewards fast repayment, not punishes it.

Conclusion: Is It Worth It?

Debt consolidation is a tool, not a cure. If you have good credit (670+), it’s a powerful way to save thousands in interest and simplify your life. If your credit is fair or poor, you need to explore secured options or debt management plans. The key is honesty with yourself about your spending habits and your ability to stick to a budget. Once you choose the right path based on your actual numbers, not your hopes, you can start climbing out of the hole.

Can I get a debt consolidation loan with a 500 credit score?

It is extremely difficult to get an unsecured personal loan with a 500 credit score. Most traditional lenders reject applications below 580. Your best options are a Debt Management Plan through a credit counseling agency, a secured loan using collateral like a car or home equity, or a loan from family members. Avoid payday loans or title loans, as their interest rates can exceed 100% and trap you in deeper debt.

Does debt consolidation hurt my credit score?

Initially, yes. Applying for a new loan causes a hard inquiry, which may drop your score by 5-10 points. Additionally, opening a new account lowers the average age of your credit history. However, over time, debt consolidation can boost your score by lowering your credit utilization ratio (as credit card balances drop to zero) and ensuring consistent on-time payments on a single loan.

What is the minimum credit score for a 0% balance transfer card?

Most issuers require a credit score of 700 or higher to approve you for a 0% introductory APR balance transfer card. Some competitive offers may require scores above 720. If your score is below 700, you may still qualify for a balance transfer, but the introductory period will likely be shorter (e.g., 6-12 months) or the APR will not be 0%.

How long does it take to get approved for a debt consolidation loan?

Online lenders can provide decisions within minutes to 24 hours, with funds deposited in 1-3 business days. Traditional banks and credit unions may take 3-7 business days for processing and verification. Secured loans, such as HELOCs, can take several weeks due to appraisal and legal documentation requirements.

Is a Debt Management Plan (DMP) better than a consolidation loan?

A DMP is better if you have poor credit (below 580) or cannot qualify for a low-interest loan. DMPs negotiate lower interest rates with creditors without requiring new debt. However, DMPs typically last 3-5 years and require you to close your credit cards. A consolidation loan is faster and provides immediate access to cash, but requires good credit and discipline to avoid re-borrowing.