What Credit Score Do You Need to Get a $30,000 Loan?

Mar, 15 2026

Mar, 15 2026

Credit Score Loan Calculator

Discover how your credit score affects monthly payments for a $30,000 personal loan in Canada. Based on 2025 data from major lenders.

Key Insight: A 50-point credit score increase can save you $6,000+ in interest over 5 years.

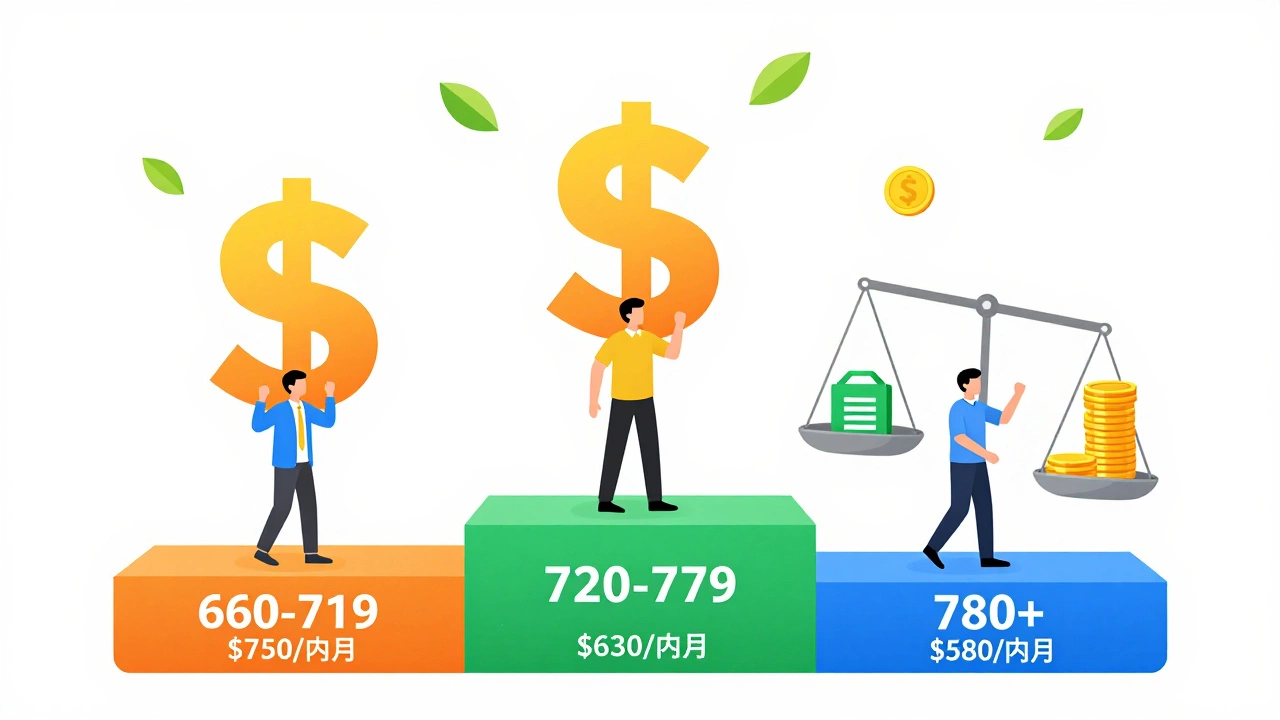

Score range guide:

660-719 = 12-18% interest

720-779 = 8-12% interest

780+ = 6-8% interest

Your Estimated Loan Terms

Monthly Payment:

Total Interest Paid:

Why This Matters

A higher credit score means lower interest rates, saving you thousands over the life of the loan. For example:

- At 660-719: You'll pay ~$15,000 in interest over 5 years

- At 720-779: You'll pay ~$5,500 in interest

- At 780+: You'll pay ~$3,500 in interest

Getting a $30,000 personal loan isn’t just about how much you earn-it’s mostly about what’s on your credit report. Lenders don’t just look at your bank balance. They want to know if you’ve paid your bills on time, how much debt you’re carrying, and whether you’ve managed credit before. If your credit score is low, you might get denied-or worse, approved with a sky-high interest rate that turns your $30,000 loan into a $50,000 repayment over time.

What credit score do lenders actually look for?

In Canada, most lenders use the FICO-equivalent score from Equifax or TransUnion, which runs from 300 to 900. For a $30,000 unsecured personal loan, you typically need a score of 660 or higher to qualify for reasonable terms. That’s the baseline. But here’s the real breakdown:

- 660-719: You’ll likely get approved, but expect interest rates between 12% and 18%. Monthly payments on a 5-year term could be around $680-$750.

- 720-779: This is the sweet spot. Lenders see you as low-risk. Rates drop to 8%-12%. Your payment drops to roughly $610-$660 per month.

- 780+: You’re in prime territory. Rates can be as low as 6%-8%. That means payments as low as $580/month. Some lenders may even waive fees or offer extended terms.

These numbers aren’t guesses. They’re based on data from Canada’s major banks and credit unions in 2025. A study by the Canadian Bankers Association showed that borrowers with scores under 660 had a 72% rejection rate on loans over $25,000. Those with scores above 720 had approval rates above 90%.

Why does your credit score matter so much?

It’s not magic. It’s math. Lenders use your score to predict how likely you are to miss a payment. A score of 700 doesn’t mean you’re rich-it means you’ve paid off credit cards, never missed a payment in 2 years, and keep your balances below 30% of your limit. That’s the pattern lenders trust.

Let’s say you’ve got $30,000 in savings but a credit score of 590. You think you’re safe. But lenders don’t care about your savings. They care about your history. If you’ve missed payments before, they assume you might again-even if you’ve got cash now.

And here’s the catch: if you’re approved with a low score, you’ll pay more in interest. Over five years on a $30,000 loan at 18%, you’ll pay nearly $15,000 in interest alone. At 7%, it’s just under $5,500. That’s almost $10,000 difference. That’s a used car. Or a vacation. Or a down payment on a new fridge.

What if your credit score is below 660?

You still have options-but they come with trade-offs.

- Get a cosigner: Someone with good credit can apply with you. Their score becomes the basis for approval. But if you miss a payment, it hits them too. This isn’t a favor-it’s a financial risk for them.

- Use collateral: Some lenders offer secured personal loans. You put up a car, savings account, or even a GIC as security. Rates drop to 9%-13%, even with a score in the 600s.

- Apply through a credit union: Credit unions often look beyond the score. They’ll check your employment history, how long you’ve been a member, and whether you’ve been saving with them. If you’ve been depositing $200/month for two years, they might approve you even with a 610 score.

- Improve your score first: If you can wait 3-6 months, focus on paying down credit card balances, disputing errors on your report, and never missing a due date. A 50-point jump can cut your interest rate in half.

What else do lenders check besides your score?

Your credit score is the gatekeeper, but it’s not the whole story. Lenders also look at:

- Debt-to-income ratio: If you’re making $60,000 a year but already owe $25,000 in car payments and student loans, they’ll worry you can’t handle another $600/month. Aim for a DTI under 40%.

- Employment stability: Have you been at the same job for 2+ years? That matters more than your job title. Freelancers need 2 years of tax returns.

- Loan purpose: Lenders like loans for debt consolidation, home repairs, or medical bills. They’re wary of loans for vacations, gambling, or crypto.

- Existing relationships: If you’ve had a chequing account with the bank for 5 years and always keep a balance, they’re more likely to approve you.

How to check your credit score for free in Canada

You don’t need to pay for this. Every Canadian has the right to one free credit report per year from each bureau. But you can get updates more often:

- Equifax Canada: Free monthly updates through their Equifax Credit Monitoring service.

- TransUnion: Offers free monthly scores via their TransUnion Credit Monitoring.

- Deserve and Credit Karma: These apps pull data from TransUnion and show real-time changes.

Check your report for errors. A $1,200 medical bill that was reported twice? A late payment from 2019 that you paid off? Those can drag your score down. Disputing them can raise your score by 40-80 points in 30 days.

Real-world example: Maria’s story

Maria, 34, lives in Toronto. She wanted a $30,000 loan to fix up her home after a basement flood. Her credit score was 640. She had steady work as a teacher, no other debt, and $5,000 in savings. She applied to three banks. Two denied her. The third approved her at 15.5% interest-$710/month for 5 years.

She was upset. So she paid off her two credit cards, kept her balances under 10%, and checked her report. She found a duplicate entry from an old utility bill. She disputed it. Three weeks later, her score jumped to 715. She reapplied. This time, she got 8.9% interest. Her payment dropped to $615. She saved $6,000 in interest.

That’s the power of knowing your score and fixing what’s wrong.

What happens if you get denied?

Don’t panic. Don’t apply to 5 lenders in a week. Each hard inquiry drops your score by 5-10 points. Instead:

- Ask the lender why you were denied. They’re required to tell you.

- Check your credit report for errors.

- Wait 3-4 months. Pay down debt. Keep all payments on time.

- Try a credit union or online lender like Borrowell or Fairstep-they use different models and are more flexible.

Final tip: Don’t chase the highest loan amount

Just because a lender says you qualify for $30,000 doesn’t mean you should take it. Ask yourself: Do I really need this? Can I afford the payment? What if I lose my job?

A $30,000 loan at 8% is manageable. At 18%, it’s a trap. The goal isn’t to get approved-it’s to get approved on terms you can live with for the next 5 years.

Can I get a $30,000 loan with a credit score of 600?

Yes, but it’s hard. Most banks will deny you. Some credit unions or online lenders might approve you if you have a cosigner, collateral, or a long history with them. Expect interest rates between 16% and 22%. Monthly payments will be high, and the total cost of the loan could exceed $50,000 over 5 years. It’s better to work on improving your score first.

How long does it take to improve a credit score?

You can see small improvements in 30 days by paying down credit card balances and fixing report errors. For a significant jump-say from 620 to 700-it usually takes 4-8 months of consistent on-time payments, low credit usage, and avoiding new debt. There’s no quick fix, but the progress is real.

Does applying for multiple loans hurt my credit?

Yes, but not as much as you think. Each hard inquiry lowers your score by 5-10 points. If you apply to 3-4 lenders within a 30-day window, credit bureaus treat it as one shopping event. So don’t spread applications out over months. Get quotes fast, then pick one.

Is a $30,000 loan too much to take on?

It depends on your income and expenses. If you earn $70,000 or more and have no other debt, it’s manageable. If you’re making $45,000 with car payments and rent already eating up half your income, it’s risky. A good rule: your total monthly debt payments shouldn’t exceed 36% of your gross income. For a $30,000 loan at 8%, that means you need at least $55,000 in annual income to feel safe.

Can I get a $30,000 loan without a credit history?

It’s very difficult. Lenders need to see how you handle credit. If you’ve never had a credit card or loan, you’re considered "credit invisible." Your best bet is to start small: get a secured credit card, use it for one monthly bill, pay it off in full, and wait 6-12 months. Then reapply.