What Is the 40-40-20 Budget Rule and How It Helps You Manage Debt

Feb, 9 2026

Feb, 9 2026

40-40-20 Budget Calculator

Your take-home pay is what you receive after taxes and deductions

How This Works

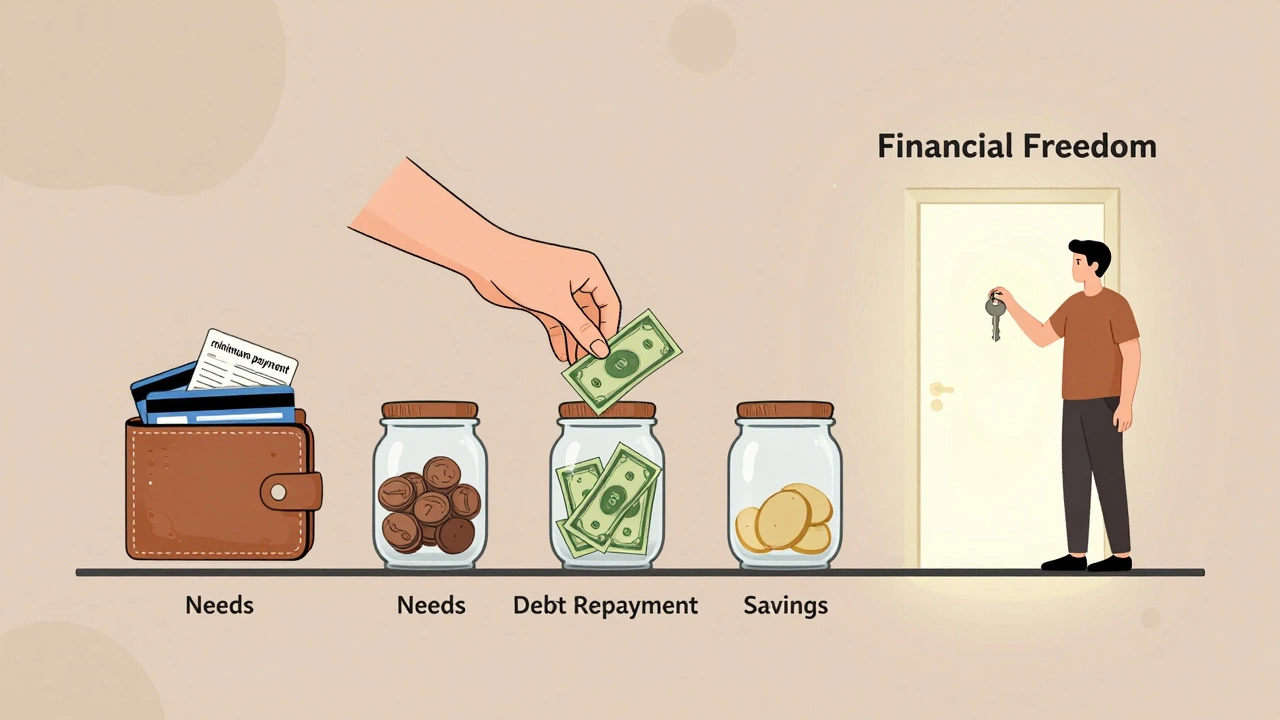

The 40-40-20 rule divides your income into three clear buckets:

- 40% Needs $0

- 40% Debt Repayment $0

- 20% Savings & Goals $0

Your Budget Allocation

Needs

Rent, groceries, utilities, minimum debt payments

Debt Repayment

Extra payments beyond minimums on credit cards and loans

Savings & Goals

Emergency fund, retirement, vacation fund

Ever feel like no matter how much you earn, you’re always running out of money before the month ends? You’re not alone. Many people struggle with budgeting because they’re using rules that don’t match real life. That’s where the 40-40-20 budget rule comes in - a simple, practical way to divide your take-home pay so you can pay down debt, save for the future, and still live comfortably.

What the 40-40-20 Rule Actually Means

The 40-40-20 budget rule breaks your monthly take-home pay into three clear buckets:

- 40% for needs - rent, groceries, utilities, insurance, minimum debt payments

- 40% for debt repayment - extra payments beyond minimums on credit cards, loans, medical bills

- 20% for savings and goals - emergency fund, retirement, vacation, big purchases

This isn’t just another budgeting trend. It’s a direct response to how most people fail: they pay minimums on debt while pretending they’re saving. The 40-40-20 rule forces you to tackle debt head-on without starving yourself.

Why This Rule Works Better Than 50/30/20

You’ve probably heard of the 50/30/20 rule: 50% needs, 30% wants, 20% savings. Sounds nice - until you have $15,000 in credit card debt at 22% interest. In that case, 30% for wants is a luxury you can’t afford. The 40-40-20 rule flips the script. It assumes you’re serious about getting out of debt, not just managing it.

Here’s the problem with 50/30/20: it lets you keep spending on non-essentials while debt grows. The 40-40-20 rule says: if you’re carrying high-interest debt, your ‘wants’ category should be zero - until the debt is gone. That 40% for debt repayment isn’t optional. It’s your priority.

How to Apply the 40-40-20 Rule Step by Step

Let’s say your monthly take-home pay is $4,000. Here’s how you’d split it:

- Calculate your take-home pay - not your gross salary. Use what actually hits your bank account after taxes and deductions.

- Track your needs - list everything you must pay to keep your life running. Rent, groceries, gas, phone bill, minimum loan payments. Total them up. If it’s more than $1,600 (40%), you’ll need to cut back.

- Allocate 40% to debt - that’s $1,600. Pay this toward your highest-interest debt first. Don’t just make minimum payments. This is where you break the cycle.

- Save 20% - $800 - split this between emergency savings and long-term goals. Even if you can only put $200 in savings this month, start somewhere.

Example: Maria earns $3,500/month. Her needs (rent, food, utilities, car insurance) total $1,400. That’s 40%. She puts $1,400 toward her $12,000 credit card debt. She saves $700. She’s not living paycheck to paycheck anymore. She’s winning.

What Counts as a Need vs. Debt Payment

People get confused here. A need is something you can’t live without. Debt repayment isn’t a need - it’s a financial obligation. But under the 40-40-20 rule, it’s treated like one because it’s costing you more than it should.

Here’s what belongs in each bucket:

| Bucket | Includes | Excludes |

|---|---|---|

| 40% Needs | Rent, utilities, groceries, basic transportation, health insurance, minimum debt payments | Streaming services, gym memberships, eating out, luxury items |

| 40% Debt Repayment | Extra payments on credit cards, personal loans, medical debt, student loans | Minimum payments only, car lease payments (unless they’re part of your debt strategy) |

| 20% Savings & Goals | Emergency fund, retirement account, vacation fund, home down payment | Impulse buys, subscriptions, gifts, entertainment |

Notice something? The 40% debt bucket doesn’t care if your debt is ‘good’ or ‘bad.’ Credit card debt? Pay it off. Medical bills? Pay them off. Student loans? Pay them off. The goal is to eliminate all high-interest obligations as fast as possible.

When the 40-40-20 Rule Doesn’t Work

This rule isn’t magic. It won’t help if:

- Your income is too low to cover 40% needs - then you need to increase income or reduce housing costs

- You’re not tracking spending - if you don’t know where your money goes, no budget will work

- You’re ignoring side income - freelance work, selling stuff, gig jobs - all of it should go to debt or savings

- You think you can ‘do it later’ - the longer you wait, the more interest piles up

If you’re making under $30,000 a year and rent takes up 50% of your income, the 40-40-20 rule won’t fit. You need to move, get a roommate, or find a second income first. This rule assumes you have some flexibility. If you don’t, start with debt snowballing or negotiate lower payments.

Real-Life Results: Who’s Using This?

People who use this rule consistently see results in 12-24 months. One Reddit user paid off $28,000 in debt in 18 months using this method. She worked two part-time jobs and put every extra dollar into debt. Her savings account grew slowly - but it grew. She didn’t have to wait until she was ‘financially ready’ to start.

Another couple in Ohio cut their credit card debt from $18,000 to $0 in 14 months. They stopped eating out, canceled all subscriptions, and used the 40% debt payment to pay off the card with the highest interest first. They didn’t feel deprived - they felt in control.

What Happens After You Pay Off the Debt?

Once your debt is gone, you don’t stop. You shift that 40%.

Now you have:

- 40% needs

- 40% savings and investments

- 20% for wants

That’s the real win. You’re no longer trapped. You’ve traded debt stress for financial freedom. You can start investing, building wealth, or even taking a real vacation without guilt.

Common Mistakes People Make

- Putting minimum payments in the debt bucket - that’s not enough. You need to pay more.

- Using windfalls (tax refunds, bonuses) for wants - they should go to debt or savings.

- Ignoring small debts - even $500 in medical bills can block your progress.

- Not adjusting when income changes - if you get a raise, increase your debt payment, not your spending.

One person I know got a $5,000 bonus and bought a new TV. Two years later, she still had $10,000 in debt. She didn’t understand that the 40-40-20 rule isn’t about being perfect - it’s about being consistent.

Start Today - No Perfect Time Exists

You don’t need to wait for a new month. Start with what you have right now. Open your bank statement. Add up your take-home pay. Calculate 40%, 40%, and 20%. Move money into separate accounts if you can. Even if you can’t pay the full 40% to debt yet, do what you can. Then increase it next month.

The 40-40-20 rule isn’t about restriction. It’s about clarity. It tells you exactly where your money should go - so you stop guessing and start winning.