What Would Payments Be on a $5000 Personal Loan? Monthly Breakdown with Real Rates

Dec, 21 2025

Dec, 21 2025

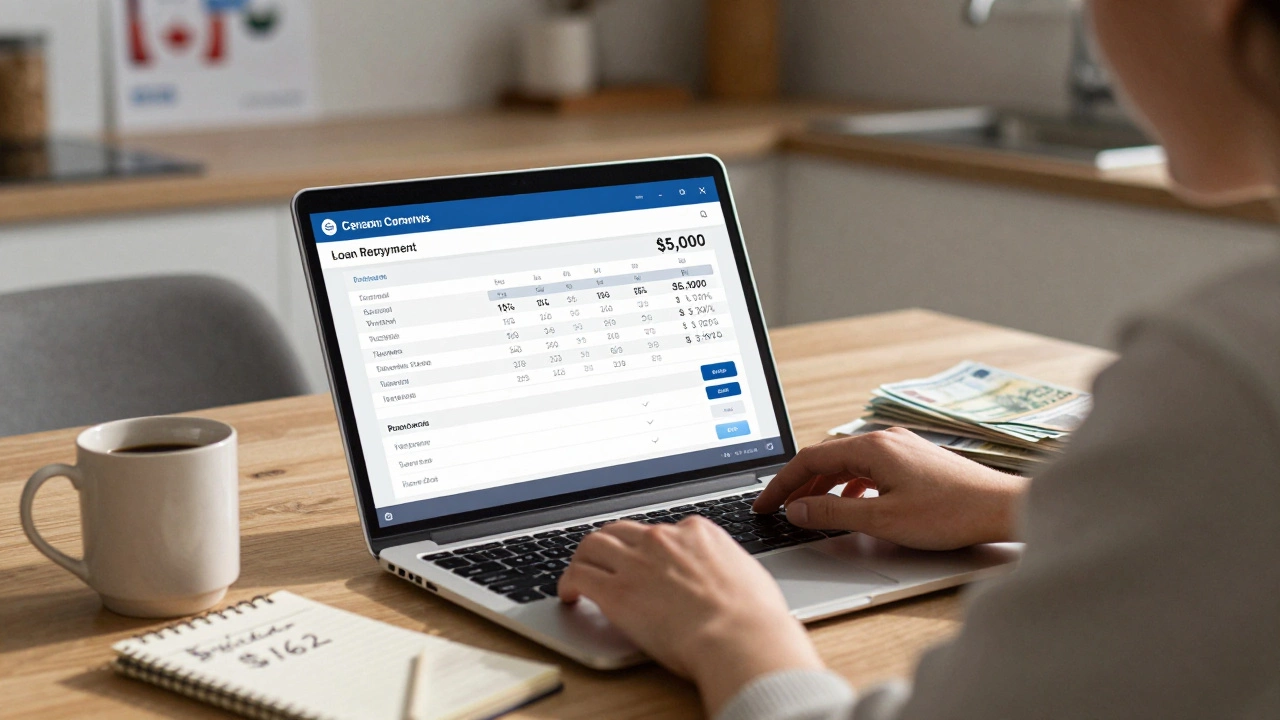

Personal Loan Calculator: $5,000 Loan Breakdown

Calculate Your Monthly Payment

See how different interest rates and loan terms affect your monthly payments on a $5,000 personal loan.

Rates based on Canada's current market as of late 2025

Your Estimated Payments

The calculator shows estimates based on current Canadian lending rates. Your actual rate may vary based on your credit score, lender, and other factors.

If you're looking at a $5,000 personal loan, you're not alone. Thousands of people in Canada take out loans of this size every year-to cover unexpected car repairs, medical bills, home improvements, or even to consolidate high-interest credit card debt. But what does that actually mean for your wallet? How much will you pay each month? And how much extra will you end up paying in interest?

The answer isn’t one number. It depends on your interest rate, how long you take to pay it back, and your credit score. Let’s break it down with real numbers you can use today.

Monthly Payments on a $5,000 Personal Loan: The Big Picture

Most personal loans in Canada for $5,000 come with terms between 12 and 60 months. Shorter terms mean higher monthly payments but less total interest. Longer terms lower your monthly bill but cost you more over time.

Here’s what your monthly payment might look like at different interest rates and terms, based on current rates as of late 2025:

| Loan Term | 6% Interest | 10% Interest | 15% Interest | 20% Interest |

|---|---|---|---|---|

| 12 months | $425 | $435 | $447 | $460 |

| 24 months | $218 | $230 | $245 | $261 |

| 36 months | $148 | $162 | $179 | $197 |

| 48 months | $117 | $132 | $151 | $171 |

| 60 months | $96 | $113 | $134 | $155 |

At 6% interest over 36 months, you’d pay about $148 a month and $6,734 total-$1,734 in interest. At 20%, you’d pay $197 a month and $7,092 total-$2,092 in interest. That’s nearly $360 more in interest just because your rate was higher.

What Determines Your Interest Rate?

Your credit score is the biggest factor. If you’ve got a score above 700, you’re likely to get rates between 6% and 10%. That’s the sweet spot. If your score is between 600 and 699, you’ll probably see 10% to 15%. Below 600? You might be looking at 15% to 20% or even higher.

But credit score isn’t the only thing lenders look at. They also check your income, existing debt, and employment history. If you’ve got a steady job and low debt-to-income ratio, you can often qualify for better rates-even if your credit isn’t perfect.

Some lenders offer lower rates if you sign up for automatic payments. It’s usually a 0.25% to 0.5% discount. That might not sound like much, but on a $5,000 loan over five years, it can save you $40 to $80 in interest.

Where to Get a $5,000 Personal Loan in Canada

You’ve got options. Banks, credit unions, online lenders, and even some fintech apps all offer personal loans. Each has trade-offs.

- Banks like RBC, TD, or Scotiabank usually offer the lowest rates-if you’re an existing customer with good credit. But their approval process can be slow, and they’re strict about income requirements.

- Credit unions often have more flexible rules and lower fees. They’re great if you’ve got a decent credit score but not a perfect one. Rates can be competitive, especially if you’ve been a member for years.

- Online lenders like LoansCanada, Borrowell, or Credibl can approve you in minutes. They’re ideal if you need money fast or have a lower credit score. But their rates can be higher, and some charge origination fees.

- Peer-to-peer lenders are less common in Canada but can be an option if traditional lenders turn you down. Rates vary widely.

One thing to watch out for: hidden fees. Some lenders charge application fees, origination fees (up to 5%), or prepayment penalties. Always read the fine print. A $5,000 loan with a 2% origination fee means you only get $4,900-but you still pay interest on the full $5,000.

What Happens If You Can’t Afford the Payments?

Missing a payment hurts your credit score-and can trigger late fees. Most lenders charge $25 to $50 per missed payment. If you fall behind, collections can start after 30 to 60 days.

If you’re struggling, don’t ignore it. Many lenders offer hardship programs. You might be able to defer a payment, extend your term, or switch to a lower monthly amount. But you have to ask. Don’t wait until you’re three months behind.

Also, think about whether you really need the loan. Could you cover the expense with savings? Or by adjusting your budget? A $5,000 loan might seem small, but adding $1,000 to $2,000 in interest over time can make a big dent in your finances.

Is a $5,000 Personal Loan Right for You?

It can be a smart move-if you use it wisely. Here’s when it makes sense:

- You have a clear, necessary expense-like fixing your car to keep your job.

- You’re consolidating higher-interest debt (like credit cards at 20%+).

- You have a plan to pay it off on time and can afford the monthly payment without stretching your budget.

Here’s when to think twice:

- You’re using it for a vacation, new clothes, or non-essential spending.

- Your income is unstable or you already have other debt payments eating up more than 40% of your take-home pay.

- You’re tempted by a longer term just to lower the monthly payment, without thinking about the total cost.

Remember: a personal loan isn’t free money. It’s a promise to pay back more than you borrowed. Make sure the cost fits your life-not the other way around.

How to Get the Best Deal on a ,000 Loan

Don’t just accept the first offer. Here’s how to shop smart:

- Check your credit report for free through Equifax or TransUnion. Fix any errors before you apply.

- Use a loan comparison tool like Borrowell or Ratehub to see pre-approved rates without hurting your credit score.

- Apply to at least three lenders. Compare not just the interest rate, but the total cost, fees, and repayment flexibility.

- Ask about discounts-for automatic payments, direct deposit, or being a long-time customer.

- Read the fine print on prepayment penalties. You should be able to pay off your loan early without extra charges.

Even a 1% lower interest rate on a $5,000 loan over 36 months saves you about $80 in interest. That’s a free $80.

What to Do After You Get the Loan

Once you’ve got the money, treat it like a serious financial commitment.

- Set up automatic payments so you never miss one.

- Keep your loan balance visible in your budgeting app (like YNAB or Mint).

- If you get a bonus, tax refund, or side income, consider putting extra toward the principal. That cuts your interest and shortens your term.

- Don’t take on new debt while paying this off. It’s easy to fall into a cycle.

Pay it off faster if you can. Even adding $50 a month to your payment on a 36-month loan at 10% interest cuts your term by almost a year and saves you $200 in interest.

How much is the monthly payment on a $5,000 personal loan?

It depends on your interest rate and loan term. At 10% interest over 36 months, your monthly payment would be about $162. At 6% over 60 months, it drops to $96. Rates and terms vary by lender and credit score.

Can I get a $5,000 personal loan with bad credit?

Yes, but expect higher interest rates-often between 15% and 25%. Some online lenders specialize in bad-credit loans, but watch for fees. Credit unions may offer better terms than banks if you’ve been a member for a while.

Is a $5,000 personal loan a good idea?

It’s a good idea if you’re using it for a necessary expense and can afford the monthly payments. It’s a bad idea if you’re using it to fund lifestyle spending or if your debt-to-income ratio is already high. Always calculate the total cost, not just the monthly payment.

How long does it take to get a $5,000 personal loan?

Online lenders can approve you in minutes and deposit funds within 24 hours. Banks and credit unions may take 1 to 5 business days. Approval speed depends on your credit history and how quickly you provide documents.

Do I need collateral for a $5,000 personal loan?

No, most $5,000 personal loans are unsecured. That means you don’t need to put up your car or home as collateral. But if you default, your credit score will take a hit, and the lender can send your debt to collections.

Can I pay off a $5,000 personal loan early?

Yes, and you should-if you can. Most Canadian lenders don’t charge prepayment penalties on personal loans. Paying early reduces your total interest and frees up your budget faster.

What’s the lowest interest rate on a $5,000 personal loan?

The lowest rates are around 6% to 7%, but they’re only available to borrowers with excellent credit (750+), stable income, and low debt. If you’re not in that group, expect rates between 10% and 15%.

Final Thoughts

A $5,000 personal loan can be a helpful tool-but only if you treat it like one. It’s not a gift. It’s a financial obligation with real consequences. The difference between a 6% and a 20% rate isn’t just numbers on a page. It’s hundreds of dollars you could’ve kept. It’s months of stress you could’ve avoided.

Know your credit score. Compare offers. Understand the total cost. And don’t rush into a loan just because you can get approved. Take the time to make sure it’s the right move-for your wallet, your peace of mind, and your future self.