Which Banks Offer 7% Interest on Savings Accounts in Canada (2026)?

May, 28 2026

May, 28 2026

Canadian Savings Rate & Real Return Calculator (2026)

Estimate your actual purchasing power growth by comparing current HISA rates against inflation.

Your Annual Breakdown

- Nominal Interest Earned: $0.00

- Inflation Cost (Loss of Purchasing Power): -$0.00

- Real Return (Actual Growth): $0.00

You are scrolling through your banking app, looking at a balance that hasn't moved much since January. You hear whispers online about 7% interest rates. It sounds like a dream come true for anyone trying to build an emergency fund or save for a down payment. But here is the hard truth: if you are sitting in Toronto, Calgary, or Vancouver, finding a bank offering a guaranteed 7% annual percentage yield (APY) on a standard savings account in May 2026 is nearly impossible.

That number belongs to the past-or perhaps to a different country entirely. In Canada, the Bank of Canada’s policy rate has stabilized, and while it is higher than the near-zero days of the early 2020s, it isn't high enough to support 7% returns on low-risk deposits. However, don't close this tab yet. While 7% might be off the table, you can still find rates between 4.5% and 5.5% with the right strategy. Let's break down where your money actually goes, why those headline-grabbing numbers exist, and how you can maximize what you earn without taking unnecessary risks.

The Reality Check: Why 7% Is Rare in Canada

To understand why you aren't seeing 7% offers from major institutions like RBC, TD, or Scotiabank, we have to look at how interest rates work. Banks make money by lending out your deposits at a higher rate than they pay you. When the central bank raises rates, borrowing becomes expensive, so banks raise their deposit rates to attract cash. When rates stabilize or drop, deposit rates follow suit.

In 2023 and early 2024, some online-only challenger banks briefly offered promotional rates touching 5% or slightly above. But 7%? That usually signals one of two things:

- It is a US-based offer: If you see a website advertising 7% APY, check the footer. Most likely, it requires a US bank account and tax ID. Many American fintech apps and credit unions pushed rates high during the inflation surge, but even there, rates have cooled down by mid-2026.

- It is a GIC, not a savings account: Guaranteed Investment Certificates (GICs) lock your money away for a set period. Some short-term GICs may have flirted with higher rates, but they are not liquid savings accounts.

Trying to force your Canadian dollars into a US-based high-yield account exposes you to currency conversion fees and exchange rate risk. The CAD/USD fluctuation could easily wipe out any extra interest you thought you were earning. Stick to Canadian-domiciled institutions to avoid hidden costs.

Where to Find the Best Rates Right Now

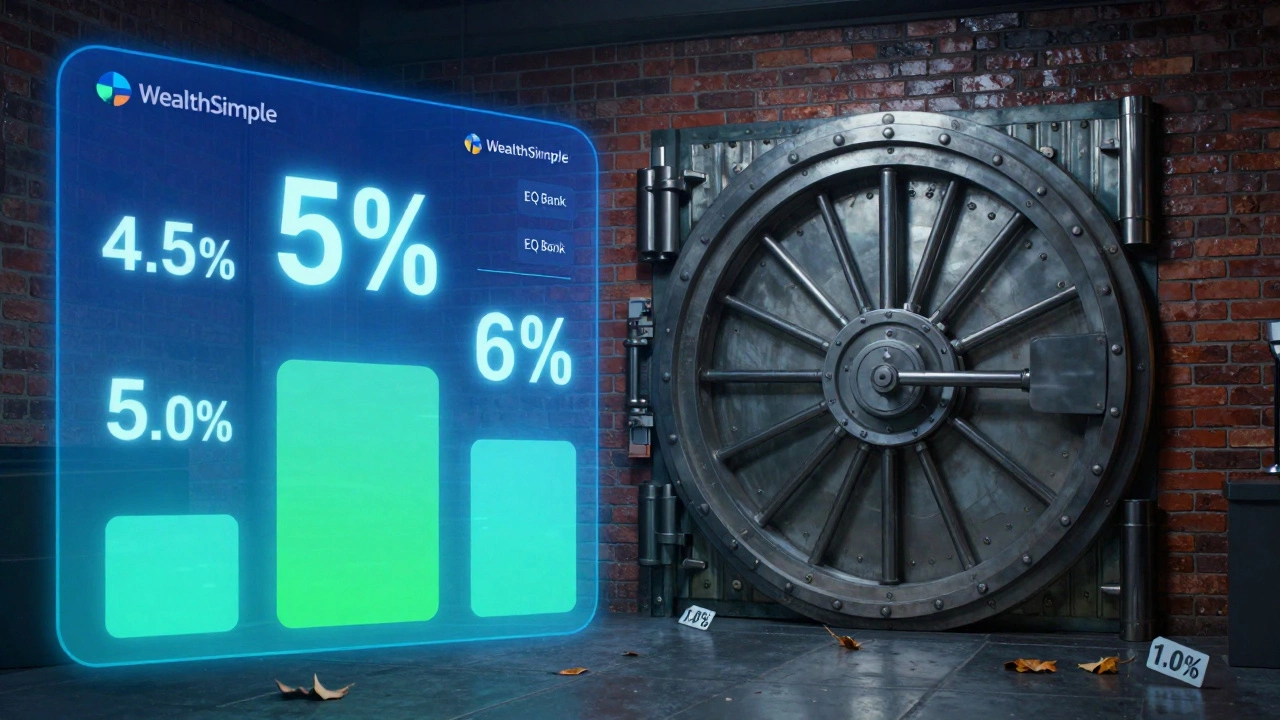

If 7% is a myth, what is the ceiling? As of May 2026, the top tier of High-Interest Savings Accounts (HISAs) in Canada sits around 4.5% to 5.0%. These are offered primarily by digital-first banks and credit unions that don't have the overhead of physical branches.

| Provider Type | Typical Rate Range | Liquidity | Best For |

|---|---|---|---|

| Big Five Banks (RBC, TD, etc.) | 1.0% - 2.0% | High | Convenience, not growth |

| Digital Banks (Wealthsimple, EQ Bank) | 4.5% - 5.0% | High | Emergency funds, short-term goals |

| Credit Unions (Desjardins, MCAP) | 4.0% - 4.8% | Medium-High | Local community support, solid rates |

| Short-Term GICs | 4.2% - 5.2% | Low (Locked) | Predictable income, no market risk |

Notice the gap. Leaving your money in a traditional checking account at a big bank is essentially losing purchasing power to inflation. Moving it to a HISA at a digital provider instantly doubles or triples your return. This is the easiest win in personal finance right now.

HISA vs. GIC: Choosing Your Strategy

You might wonder if locking your money away in a GIC is worth it to chase that extra tenth of a percent. Here is how to decide:

High-Interest Savings Accounts (HISAs) are liquid deposit accounts that pay competitive interest rates and allow withdrawals without penalty. They are perfect for your emergency fund. Life happens. You need that car repaired, or you lose your job. With a HISA, you can access your cash instantly via Interac e-Transfer or debit card. The trade-off is that the rate can change at any time. If the Bank of Canada cuts rates next month, your 5% could drop to 4% overnight.

Guaranteed Investment Certificates (GICs) are fixed-income investments where you lend money to a bank for a set period in exchange for a guaranteed interest rate. If you know you won't touch $10,000 for six months, a GIC locks in that rate. Even if market rates crash, you keep your agreed-upon return. However, accessing the money early usually means forfeiting all interest earned, or paying a significant penalty.

A smart approach is diversification. Keep three to six months of expenses in a HISA for safety. Park longer-term savings-like a vacation fund due in a year-in a ladder of GICs. This way, you capture higher yields without sacrificing liquidity when you really need it.

The "ISA" Confusion: UK vs. Canada

The title of your search mentions "ISA accounts." This is a critical distinction. An Individual Savings Account (ISA) is a UK tax wrapper. It allows British residents to save or invest money without paying tax on the gains. Canada does not have ISAs.

If you are reading articles about ISAs offering high returns, they are referring to UK products. Trying to open a UK ISA as a Canadian resident is a logistical nightmare involving non-resident status issues and potential tax complications. Instead, focus on Canadian equivalents:

- TFSAs (Tax-Free Savings Accounts): Money grows tax-free. Withdrawals are tax-free. This is your best friend for long-term wealth building.

- RSPs (Registered Retirement Savings Plans): Contributions reduce taxable income now; growth is taxed upon withdrawal. Ideal for retirement.

You can hold high-interest savings accounts *inside* a TFSA. This means the interest you earn at that 4.5% rate is never taxed. Over ten years, that tax shield adds up to thousands of dollars. Always prioritize funding your TFSA before using a non-registered savings account.

Hidden Fees That Eat Your Interest

Before you sign up for the highest-rate account you find, read the fine print. A 5% rate looks great until you realize the account charges a monthly maintenance fee of $5 if you don't maintain a minimum balance of $10,000. Or worse, some accounts charge fees for every withdrawal over a certain limit.

Look for these red flags:

- Monthly Maintenance Fees: Avoid these unless you qualify for the waiver. They compound negatively against your interest earnings.

- Withdrawal Limits: Some HISAs cap free transactions at four per month. Exceeding this triggers a fee. Ensure this aligns with your spending habits.

- Minimum Balance Requirements: To get the advertised rate, you often need a specific balance. If you dip below it, the rate might plummet to 0.5%.

Digital banks like EQ Bank and Wealthsimple Cash typically have no monthly fees and unlimited transactions, making them cleaner options for most Canadians. Credit unions may have lower minimums but sometimes charge branch usage fees if you try to withdraw cash physically.

How to Actually Grow Your Money Faster

If 7% feels too slow, and you have a higher risk tolerance, you need to look beyond savings accounts. Savings accounts are designed for capital preservation, not growth. If you want double-digit returns, you are entering the world of investing.

Consider a portfolio of low-cost ETFs (Exchange-Traded Funds). Historically, the stock market averages 7-10% annual returns over long periods, though with volatility. You could have a bad year where you lose 10%, followed by a year where you gain 20%. A savings account will never do that. It will just sit there, slowly growing.

For many people, the hybrid approach works best:

- Step 1: Build a fully funded emergency fund in a HISA (4.5-5%).

- Step 2: Max out your TFSA contribution room.

- Step 3: Inside the TFSA, allocate based on timeline. Short-term goals stay in cash/GICs. Long-term goals (retirement, house down payment in 5+ years) go into diversified ETFs.

This strategy protects your downside while giving you exposure to upside growth. It is boring, disciplined, and effective.

Common Mistakes to Avoid

I talk to plenty of friends in Toronto who fall into the same traps. Don't be one of them.

Mistake 1: Chasing Promotional Rates. Some banks offer 6% for the first 90 days, then drop to 1%. This is a customer acquisition tactic. Unless you are willing to move your money every quarter, these rates are misleading. Calculate the weighted average over a year, not just the headline number.

Mistake 2: Ignoring Inflation. If inflation is running at 3% and your savings account pays 2%, you are technically losing money. Your purchasing power shrinks. Always ensure your nominal rate exceeds the current CPI (Consumer Price Index) inflation rate. In 2026, with inflation stabilizing around 2-3%, a 4.5% HISA gives you a positive real return. That is the goal.

Mistake 3: Using Non-Insured Institutions. Only use banks and credit unions insured by CDIC (Canada Deposit Insurance Corporation) or provincial equivalents. This guarantees your principal up to $100,000 per category if the institution fails. Never put life savings in a shady offshore broker promising 10% returns.

Next Steps for Your Wallet

So, which bank is giving 7%? None in Canada, reliably. But you don't need 7% to win. You need consistency and efficiency. Open a high-interest savings account at a reputable digital provider today. Link it to your primary chequing account. Set up an automatic transfer of whatever amount you can spare each payday.

Watch that balance grow. Reinvest the interest. And remember, the best financial decision is often the simplest one: stop letting your money sleep in a zero-percent account. Wake it up, move it to a better environment, and let compound interest do the heavy lifting. You might not hit 7%, but you will certainly beat the alternative.

Are there any Canadian banks offering 7% interest on savings accounts in 2026?

No, there are currently no legitimate Canadian banks offering a guaranteed 7% interest rate on standard savings accounts. The highest rates available from reputable digital banks and credit unions range between 4.5% and 5.0%. Offers claiming 7% are likely from US-based institutions, involve significant risk, or are misleading promotional rates that drop quickly.

What is the difference between a HISA and a GIC?

A High-Interest Savings Account (HISA) offers liquidity, meaning you can withdraw your money at any time without penalty, but the interest rate can change. A Guaranteed Investment Certificate (GIC) locks your money for a fixed term (e.g., 6 months, 1 year) in exchange for a guaranteed interest rate. Early withdrawal from a GIC usually results in a loss of interest or penalties.

Can I open a UK ISA as a Canadian resident?

Generally, no. Individual Savings Accounts (ISAs) are tax wrappers designed for UK taxpayers. As a Canadian resident, you would not benefit from the tax advantages and could face complex reporting requirements. Instead, utilize Canadian registered accounts like TFSAs and RSPs for tax-efficient saving and investing.

Is my money safe in a high-interest savings account?

Yes, provided the institution is member-insured. In Canada, look for CDIC (Canada Deposit Insurance Corporation) coverage for banks or provincial insurance for credit unions. This protects your principal up to $100,000 per account category if the financial institution fails. Always verify insurance status before depositing funds.

Should I put my emergency fund in a HISA or a GIC?

You should keep your emergency fund in a High-Interest Savings Account (HISA). Emergency funds require immediate accessibility. GICs lock your money away, and breaking them early often incurs penalties that negate the higher interest rate. The slight rate difference is not worth the risk of inaccessible cash during an emergency.