Which Four Banks Are in Trouble? What This Means for Your Savings Accounts in 2026

Jun, 4 2026

Jun, 4 2026

Bank Risk Assessment Tool

Follow these steps to determine if your current bank fits one of the four "trouble profiles" identified for 2026.

Step 1: Identify Your Bank's Type

Which description best matches your primary bank?

Regional Bank

Mid-sized ($10B-$50B assets), heavy focus on local commercial real estate or office buildings.

Digital Neobank

App-only, fintech startup, relies on venture capital rather than traditional deposits.

Large National Bank

Major institution with physical branches, diversified revenue streams, "too big to fail" status.

Foreign Subsidiary

Branch of an international bank, facing new regulatory compliance rules.

Step 2: Check Interest Rate Trends

How has your bank behaved regarding interest rates recently?

Step 3: Verify Insurance Coverage

Do you know your total balance at this single institution?

Step 4: Monitor Stability Signals

Have you noticed any of these recent changes?

Your Bank Risk Assessment

It’s June 2026, and the banking headlines are getting louder. If you’ve been scrolling through your feed lately, you’ve probably seen warnings about instability, mergers, or even outright collapses. The question on everyone’s mind isn’t just "is my money safe?" but specifically, "which four banks are in trouble?"

The answer isn’t as simple as naming four specific institutions right here and now. Bank troubles shift rapidly. One week a regional lender is stable; the next, it’s facing a liquidity crisis. However, by mid-2026, patterns have emerged that point to four distinct *types* of banks currently under pressure. Understanding these categories helps you protect your savings far better than memorizing a static list of names.

Why can't I get a simple list of four failing banks?

Banking crises are dynamic. By the time an article publishes, the situation may have changed due to government bailouts, mergers, or sudden withdrawals. Instead of listing specific names that might become outdated instantly, it is safer to identify the *profiles* of banks currently at risk so you can spot them yourself.

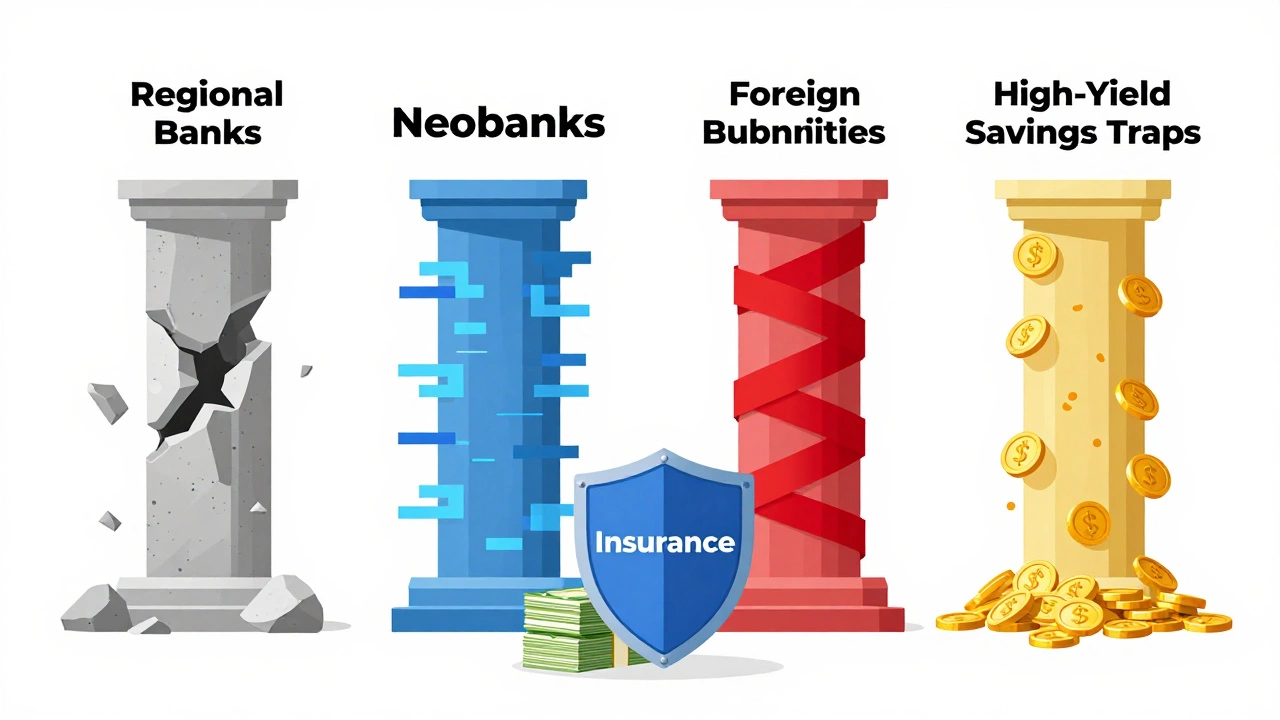

The Four Profiles of Banks Currently Under Pressure

When experts talk about "banks in trouble" in 2026, they are usually referring to institutions fitting one of these four dangerous profiles. If your current bank matches any of these descriptions, it’s time to pay attention.

- Uninsured Regional Banks with High Commercial Real Estate Exposure: These are mid-sized banks (assets between $10 billion and $50 billion) that lent heavily to office buildings and commercial properties during the boom years. As remote work remains prevalent in 2026, vacancy rates are high, and loan defaults are rising. These banks often lack the diversified funding sources of larger giants.

- Digital-Only Neobanks Without Clear Profit Models: Many fintech startups launched during the pandemic hype cycle. In 2026, those that haven’t figured out how to make sustainable profits are burning cash. They rely on venture capital rather than customer deposits. When funding dries up, they face existential threats.

- Foreign-Owned Subsidiaries Facing Regulatory Scrutiny: Some branches of international banks operating in local markets are struggling with new compliance rules introduced in 2024-2025. These rules require higher capital reserves, squeezing their margins and forcing them to raise fees or cut services.

- Banks with Rapid, Unchecked Growth in High-Yield Savings: Remember when every bank offered 5% APY? To attract deposits, some smaller banks borrowed cheaply elsewhere to pay you high interest. Now that interest rates have stabilized or risen further, their cost of funds has skyrocketed, eroding their profitability.

If your bank fits into one of these buckets, it doesn’t mean it will fail tomorrow. But it does mean it’s in the "trouble zone." Let’s look at why this matters for your savings account.

Why Your Savings Account Is the First Place to Check

You might think, "I’m not a shareholder, so why should I care if a bank is struggling?" Here’s the thing: when a bank gets into trouble, it often tries to stop the bleeding by cutting costs. Who pays the price? You do.

Before a bank fails, it might:

- Raise minimum balance requirements.

- Add monthly maintenance fees where there were none before.

- Reduce the interest rate on your savings account to near zero.

- Limit ATM access or charge for basic transactions.

In extreme cases, if the bank collapses, you lose access to your money immediately. Even if you get it back later, the hassle is immense. That’s why knowing which banks are vulnerable is crucial for anyone who values peace of mind.

How to Spot Trouble Before It Hits

You don’t need a finance degree to check if your bank is healthy. There are three simple signals you can monitor right now.

1. The Deposit Insurance Limit

This is the most critical rule. In Canada, the Canada Deposit Insurance Corporation (CDIC) protects eligible deposits up to $100,000 CAD per account category. In the US, the Federal Deposit Insurance Corporation (FDIC) offers the same $250,000 USD coverage.

If you have more than this limit in a single bank, you are exposed. Period. No matter how "stable" the bank seems, amounts above the insurance cap are at risk. Spread your money across multiple insured institutions if you hold large sums.

2. Interest Rate Behavior

Healthy banks adjust their savings rates based on market conditions. If your bank suddenly slashes its interest rate while competitors keep theirs steady, it could be a sign they are trying to discourage new deposits because they are short on cash. Conversely, if a small bank offers an unusually high rate compared to major banks, ask yourself: why are they paying so much? Often, it’s because they are desperate for liquidity.

3. News and Rumors

Pay attention to news about mergers. A merger isn’t always bad, but if a bank is being acquired by a larger competitor, it’s often because the smaller bank couldn’t survive alone. Also, watch for executive departures. If the CEO and CFO leave within weeks of each other, something is wrong behind the scenes.

| Red Flag (Trouble) | Green Light (Stable) |

|---|---|

| Sudden fee increases | Transparent, consistent pricing |

| Interest rates lagging behind inflation/market | Competitive rates aligned with central bank policy |

| Frequent software glitches or app downtime | Reliable digital platform |

| Lack of recent financial reporting | Regular publication of quarterly results |

What to Do If Your Bank Is in the "Trouble Zone"

Don’t panic. Panicking causes bank runs, which actually makes the problem worse. Instead, take calculated steps to secure your finances.

- Verify Your Insurance Coverage: Log in to your bank’s website and check your CDIC/FDIC status. Make sure your account types are eligible. Note that investment accounts (like stocks or mutual funds) are NOT covered by deposit insurance.

- Diversify Your Deposits: If you have $150,000 in one troubled bank, move $50,000 to a different, well-established institution. Keep your total exposure below the insurance limit at any single place.

- Switch to a "Too Big to Fail" Bank or Credit Union: Large national banks and established credit unions have stronger backing and easier access to emergency funding from central banks. They are less likely to face sudden insolvency.

- Monitor Communications: Sign up for email alerts from your bank. If they announce changes to terms and conditions, read them carefully. Look for hidden fees or reduced benefits.

The Bigger Picture: Why This Is Happening in 2026

The banking sector is undergoing a massive transformation. For decades, banks relied on physical branches and low-interest loans. Today, they face competition from fintechs, changing customer habits, and stricter regulations.

In 2024 and 2025, several high-profile failures shook confidence. Regulators responded by tightening rules, especially for mid-sized banks. While this makes the system safer overall, it also squeezes the margins of smaller lenders. Those that can’t adapt are the ones ending up in the "trouble" category we discussed earlier.

Additionally, the rise of digital-only banking has created a two-tier system. On one side, you have massive tech-backed platforms with huge user bases. On the other, you have traditional community banks struggling to compete on technology and convenience. The middle ground is disappearing.

Protecting Your Wealth Beyond the Bank

While keeping your savings safe is priority number one, don’t forget that inflation eats away at cash holdings. Leaving all your money in a savings account-even a safe one-means losing purchasing power over time.

Consider a balanced approach:

- Emergency Fund: Keep 3-6 months of expenses in a high-yield, insured savings account.

- Short-Term Goals: Use Guaranteed Investment Certificates (GICs) or Treasury Bills for funds you’ll need in 1-3 years. These are generally considered very safe.

- Long-Term Growth: Invest the rest in diversified portfolios (stocks, bonds, ETFs). Yes, investments carry risk, but they also offer returns that beat inflation.

Remember, diversification isn’t just for stocks. It applies to where you keep your cash too. Don’t put all your eggs in one basket, whether that basket is a single bank or a single asset class.

Final Thoughts: Stay Alert, Not Anxious

So, which four banks are in trouble? The answer depends on where you live and what type of banking you use. But the principles remain the same: avoid uninsured deposits, watch for red flags like fee hikes and rate cuts, and diversify your financial relationships.

Banking is supposed to be boring. If it feels exciting or confusing, that’s a warning sign. Take control of your money by staying informed and proactive. Your future self will thank you.

Is my money safe if my bank fails?

Yes, up to the insurance limits. In Canada, CDIC covers up to $100,000 per account category. In the US, FDIC covers up to $250,000. Amounts above these limits are at risk unless moved to another insured institution.

Should I withdraw all my money from a struggling bank?

Withdrawing everything can trigger a bank run, making the situation worse. Instead, gradually move excess funds above insurance limits to safer institutions. Keep enough for daily needs to avoid inconvenience.

Are credit unions safer than banks?

Credit unions are generally very stable because they are member-owned and non-profit. In Canada, they are covered by provincial deposit insurance plans, which often provide similar or higher protection than CDIC. Research your local credit union’s financial health.

How do I know if my online bank is legitimate?

Check if they are registered with your country’s financial regulator (e.g., OSFI in Canada, OCC in the US). Look for clear contact information, transparent fee structures, and evidence of deposit insurance. Be wary of banks offering unrealistically high interest rates.

What happens to my loans if my bank fails?

Your loans don’t disappear. They are typically transferred to another institution or taken over by regulators. You must continue making payments as scheduled. Failure to pay can damage your credit score, even if the original bank has collapsed.