Home Insurance Coverage: What’s Really Included and What’s Not

When you buy home insurance coverage, a contract between you and an insurer that protects your house and belongings against covered losses. Also known as homeowners insurance, it’s meant to be your financial safety net—but only if you know what’s actually in it. Most people think it covers everything from floods to stolen jewelry, but that’s not true. The truth is, home insurance coverage has strict limits, hidden exclusions, and fine print that can leave you exposed when you need it most.

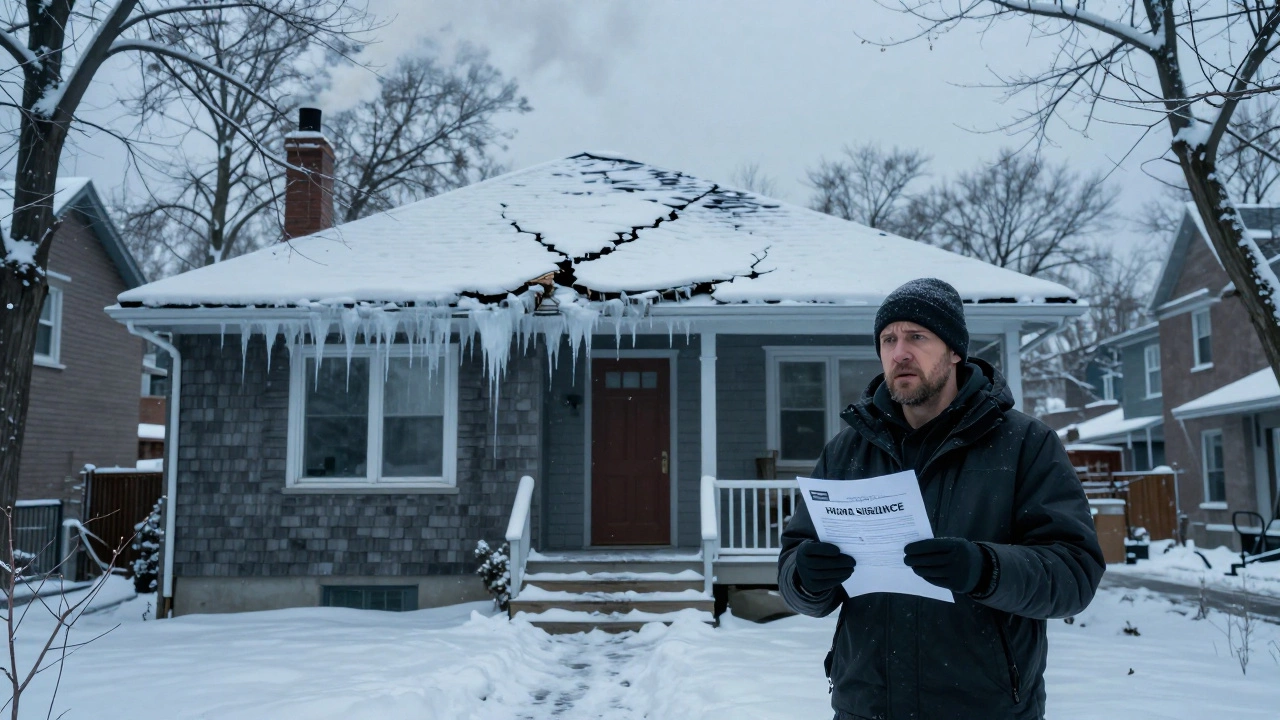

One major thing most policies cover is damage from fire, lightning, windstorms, and theft. That’s the basics. But if your roof collapses under snow, or a tree falls on your garage, your policy might pay—unless you live in a high-risk area where wind damage is excluded. Then there’s water damage. Sudden bursts from pipes? Usually covered. Slow leaks from a faulty roof? Almost always denied. And don’t assume your expensive electronics or jewelry are fully protected—those often have sub-limits. If your diamond ring is worth $5,000 but your policy only covers $1,500 for personal property, you’re out of pocket $3,500. That’s not a gap. That’s a hole.

Then there’s liability. If someone slips on your icy walkway and breaks their hip, your home insurance coverage, includes liability protection that pays for medical bills and legal costs if you’re found responsible. Also known as personal liability coverage, it’s one of the most important parts of your policy. But if you run a home business, host frequent parties, or rent out a room—even temporarily—you might be voiding that coverage. Insurers don’t care if you didn’t know. They’ll deny the claim, and you’ll be on your own.

And what about your garage? Your shed? Your fence? These are often called "other structures" and usually covered at 10% of your home’s insured value. So if your house is insured for $300,000, you get $30,000 for detached structures. Sounds like a lot—until you realize a new detached garage costs $50,000. That’s not coverage. That’s a gamble.

Home insurance coverage doesn’t just protect your house. It protects your peace of mind. But only if you understand the rules. That’s why the posts below dig into real cases: what got paid, what got denied, and how people fixed their policies before it was too late. You’ll see how one extra endorsement saved someone from losing their home after a wildfire. How another person learned their policy didn’t cover sewer backups—until it flooded their basement. And how a simple $50 add-on could have covered a $12,000 theft.

These aren’t hypotheticals. These are real stories from people who thought they were covered—until they weren’t. The posts ahead give you the exact details you need to check your own policy, ask the right questions, and avoid the traps most homeowners never see coming.

What Is Usually Covered in Home Insurance? A Clear Breakdown for Canadian Homeowners

0 Comments

Home insurance in Canada typically covers fire, theft, storms, and liability-but not floods, earthquakes, or wear and tear. Know what's included, what's excluded, and how to avoid being underinsured.

What Is the Replacement Cost Price in Home Insurance?

0 Comments

Replacement cost price in home insurance is the amount needed to rebuild your home from scratch at current prices. Learn why it matters more than market value and how to make sure you're covered.

Find out which home insurance providers in Canada offer the most reliable coverage in 2025, what to look for in a policy, and how to avoid common pitfalls that leave homeowners unprotected.